A quick overview

- Over the last ten years, Canada’s oil and gas sector has undergone a deep transformation—driven not by hype, but by necessity.

- Industry leaders like Suncor, Enbridge, and Imperial have embedded AI, automation, and digital twins to cut downtime, reduce emissions, and improve safety.

- Innovations span the full value chain—from autonomous vehicles to blockchain reporting to cleantech breakthroughs in carbon capture.

- Companies like Sanovas are bridging sectors, applying medtech precision to pipeline integrity and methane control.

- These changes are not only improving performance—they’re laying the groundwork for Canada’s net-zero ambitions.

- The innovation built for energy is now spilling into agriculture, infrastructure, and climate modeling—fueling broader economic impact.

Introduction

Over the past ten years, innovation in Canada’s oil and gas sector has evolved quietly but profoundly. While tech giants like OpenAI and Google captured the public imagination with AI breakthroughs and digital ecosystems, the Canadian energy sector was busy engineering its modification, less visible, but no less essential.

This wasn’t about overnight disruption or viral platforms. It was about building resilience in the face of market volatility, tightening regulations, environmental accountability, and shifting energy expectations. It was a reinvention grounded in necessity: smarter operations, cleaner output, sharper tools. Innovation, not as a buzzword, but as survival.

The New Oilfield: Digitized, Streamlined, Responsive

The shift wasn’t just technological. It was cultural. The sector moved from manual to machine-assisted, from reactive to predictive, from analog to digital twins. Today’s oilfield is monitored in real time, managed with precision software, and increasingly augmented by AI. Downtime is measured in milliseconds. Data is no longer a byproduct—it’s an asset.

Where OpenAI is training models to think like humans, Canadian energy firms are training systems to think like engineers. It’s a different context, but the same ambition: use data to anticipate, optimize, and act.

Companies Leading the Charge in Oil & Gas Tech Innovation

Germany: Applied Research Through Fraunhofer Institutes

Suncor has been at the forefront of automation in the oilsands. Autonomous haul trucks, advanced analytics for tailings and emissions, and digitized maintenance systems are now embedded across its operations. Their approach to innovation is integrated—less about big headlines, more about long-term performance.

So far, they have:

- Deployed autonomous haul trucks in the oilsands, cutting fuel costs, reducing maintenance, and improving safety in high-risk zones.

- Implemented AI-based predictive maintenance systems for mechanical assets, helping reduce unplanned downtime and extend asset life.

- Used data analytics to optimize tailings management, an area critical for both ESG performance and public trust.

- Invested in digital twins and simulation software to enhance scenario modeling for production planning and emissions forecasting.

Suncor isn’t just digitizing the field—they’re embedding intelligence into every layer of the operation. [1]

Enbridge: Building a Digital Nervous System for Pipelines

Enbridge has made major moves in digital pipeline monitoring and AI-driven risk modeling. From leak detection to drone-assisted inspections, their infrastructure isn’t just built to move energy—it’s designed to sense and adapt to risk in real time. They’ve also explored blockchain pilots for commodity logistics, laying the groundwork for more secure, transparent trading environments. In the past 10 years, they’ve:

- Rolled out machine learning algorithms for leak detection, making their pipeline systems safer and more responsive.

- Used drones and AI-assisted imagery to inspect hundreds of miles of pipeline for structural integrity and environmental threats.

- Piloted blockchain technology to streamline commodity logistics, improve traceability, and reduce administrative overhead in crude trading.

- Invested in automated SCADA systems (Supervisory Control and Data Acquisition), allowing for more granular control and response across their assets.

They’ve essentially built a nervous system into their pipeline network. [2]

Imperial Oil: Merging AI with Environmental Responsibility

Imperial’s Kearl operation is among Canada’s most digitally advanced oilsands sites. AI-based modeling helps optimize drilling, while emissions reduction and carbon capture are core to their technology roadmap. It’s a balance of performance and responsibility, pushed forward by serious internal R&D muscle. Key innovations include:

- Leveraging AI modeling to optimize well pad layout and drilling sequences, especially in complex oilsands environments.

- Applying remote sensing and automation at its Kearl operation to streamline production, minimize energy usage, and reduce water intensity.

- Pursuing carbon capture and storage (CCS) R&D through the Pathways Alliance, aiming to decarbonize oilsands production by 2050.

- Exploring low-emission fuel alternatives, including advanced biofuels and hydrogen pathways, to diversify energy offerings.

Imperial is pairing AI with environmental tech—building solutions that are as strategic as they are operational. [3]

Sanovas Canada: Bringing Medtech Precision to Energy Innovation

Sanovas may not be a household name in energy, but its roots in medtech give it a different kind of edge. Their tools—originally developed for high-precision medical procedures—are now being adapted for pipeline diagnostics, methane control, and microscale fluid dynamics. It’s a rare case of innovation flowing into oil & gas from outside the industry. In the last decade, they’ve translated this medical precision into industrial impact:

- Designed micro-fluidics tools for pipeline inspection and maintenance, reducing downtime and improving integrity in tight, inaccessible spaces.

- Developed methane abatement tech based on controlled fluid delivery, allowing for more effective and efficient greenhouse gas control.

- Created sensor-based diagnostics platforms capable of delivering real-time environmental and pressure data from within pipelines.

It’s a rare example of medtech crossing into energy, bringing surgical precision to one of the world’s heaviest industries. [4]

Talisman Energy (now part of Repsol): Pioneering Digital Strategy in the Field

Before its acquisition, Talisman was one of the first Canadian firms to integrate cloud-based geological modeling and data-driven field strategy. Much of that early digital thinking has since influenced Repsol’s broader innovation strategy, especially in unconventional assets. Talisman’s legacy still resonates in how smaller, agile firms think about smart field development.

During its final years, the company:

- Implemented cloud-based geological modeling to improve exploration targeting in both conventional and shale plays.

- Used digital dashboards and real-time field data to empower front-line operators with more control over daily decision-making.

- Piloted early machine learning tools to assess drilling efficiency and predict completion outcomes.

Though it no longer exists as a standalone company, its early digital strategy laid the foundation for Repsol’s broader innovation approach in North America. [5]

How Innovation is Reshaping Canada’s Oil and Gas Industry

Canada’s energy sector doesn’t move at Silicon Valley speed—and that’s not a flaw, it’s a function of scale, risk, and infrastructure. Where OpenAI builds digital intelligence, this sector builds physical resilience. Where Google refines data about clicks, the oilfield refines hydrocarbons, behavior, and real-world systems.

But the methods are beginning to echo each other. AI is no longer confined to marketing or media—it’s optimizing flow rates, predicting asset failures, and mapping subsurface anomalies. What tech does in milliseconds, oil and gas do in real-time operations with environmental and financial stakes attached.

The common denominator? Data used with intention. Models that learn. Systems that get smarter with every cycle.

Smarter Operations in High-Stakes Environments

Innovation in Canada’s oil and gas sector has taken many forms—each targeting a different pain point in the value chain.

Operational Innovation: Automating Safety and Efficiency

Operational innovations, like autonomous haul trucks and real-time asset monitoring, have improved safety and cut downtime in remote and hazardous environments.

Digital Transformation: Predictive Systems and Smart Fields

Digital innovations, including predictive maintenance systems, cloud-based drilling analytics, and AI-driven reservoir modeling, are optimizing production with unprecedented precision.

Cleantech Advances: Meeting the New Environmental Mandate

On the environmental side, cleantech innovations—from methane detection drones to advanced water recycling systems and early-stage carbon capture tech—are helping operators meet stricter sustainability benchmarks. Even logistics and compliance platforms, like digital field ticketing and blockchain-based reporting, are streamlining back-end processes that used to be bottlenecks.

Collectively, these innovations aren’t just making operations more efficient, they reshape how the entire sector responds to risk, regulation, and responsibility. In a high-stakes industry, the ability to adapt is becoming the new baseline for success.

Contribution Beyond the Sector

This isn’t just about drilling smarter. It’s about applying energy-derived innovation across other critical sectors—clean tech, water management, infrastructure, and agriculture. From pipeline sensors adapted for irrigation systems to AI platforms developed for field monitoring now used in climate modeling, the ripple effect is real.

Lest we forget emissions, many of the tools being built today—automated monitoring, methane capture, remote sensing—will be instrumental in Canada’s energy transition and net-zero targets. The sector is no longer just reacting to climate pressure; it’s building the tech to respond.

Conclusion: The Road Ahead

The next ten years won’t be about simply optimizing what exists—they’ll be about reimagining the interface between energy and the environment. There are possibilities of autonomous microgrids, intelligent emissions accounting, and integrated hydrogen and CCS hubs. The digital layer is no longer optional; it is foundational.

Canada’s oil and gas sector is well equipped, however, leadership will require more than operational upgrades. It will require strategic investment, coordinated policy, and a renewed sense of identity as producers and innovators.

Because innovation in energy doesn’t always make headlines, however, it keeps everything else running.

Sources

#EnergyInnovation #OilAndGasTech #CleanEnergySolutions #DigitalTransformation #CanadianEnergy #RDIncentives #CheckpointResearch #InnovationCanada #SmartInfrastructure #ClimateTech

At Checkpoint Research, we understand that innovation in oil and gas doesn’t always look like a lab experiment—it often lives in field upgrades, AI integrations, cleantech adaptations, and operational refinements.

We help organizations in complex industries like energy structure their SR&ED processes around real-world innovation—ensuring the work you’re already doing is properly captured, supported, and strategically aligned with funding opportunities.

If your team is building smarter systems, developing in-house solutions, or adapting tech in high-stakes environments, we can help you stay organized, compliant, and ready to claim.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

Contents

A quick overview

- Canada has strong innovation assets—like top-tier research institutions and a skilled workforce—but struggles to convert these into productivity and high-impact innovation.

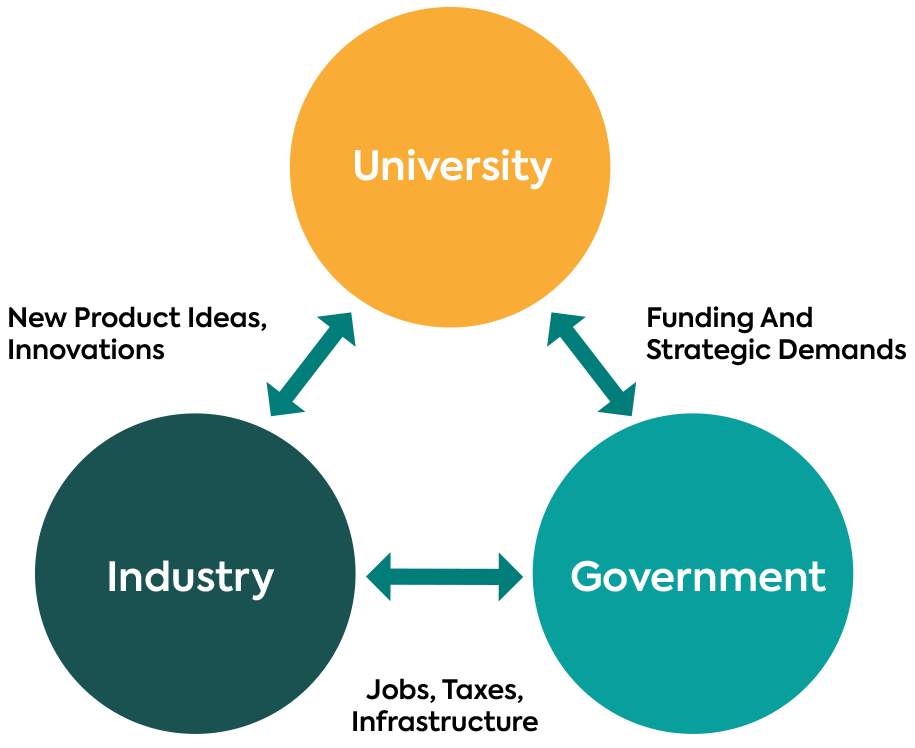

- The Triple Helix model, which promotes collaboration between government, academia, and industry, offers a strategic framework to better align efforts and support innovation-driven growth.

- Public-Private Partnerships (PPPs) in Canada need reform; current approaches are often fragmented and lack feedback loops, coordination, and long-term vision.

- Global examples from Germany, Denmark, and Singapore show how structured innovation clusters and state-supported coordination can lead to stronger commercial outcomes and global competitiveness.

- Canada’s path forward includes adopting mission-based innovation clusters, boosting translational research, modernizing procurement, and treating innovation as foundational infrastructure—not just policy.

Introduction

Our past studies have shown that Canada possesses substantial innovation assets, including a well-educated workforce, globally recognized research institutions, and a wealth of natural and technological resources. Yet, despite this strong foundation, the country continues to face structural challenges in translating these inputs into sustained, high-impact innovation as well as a higher yield in productivity.

What Is the Triple Helix Model and Why It Matters for Canada’s Innovation Ecosystem

The Triple Helix model, which emphasizes systemic collaboration among government, academia, and industry, presents a promising framework to address this gap. Countries such as Germany, Denmark, and Singapore have embraced this approach to strengthen innovation ecosystems through tightly coordinated public-private partnerships (PPPs), mission-driven research, and institutional innovation clusters. Canada has opportunities to learn from and adapt these strategies to better align public and private efforts, support knowledge translation, and increase national innovation capacity.

The Role of Public-Private Partnerships in Innovation Ecosystems

While Canada maintains numerous PPPs across research and technology domains, many are siloed, underfunded, or limited in long-term coordination. Current models often lack formal structures for feedback, performance measurement, or policy alignment.

To improve outcomes, PPPs should evolve beyond project-based collaboration into platforms for shared experimentation, risk mitigation, and applied problem-solving. This includes:

Sector-Specific Innovation Clusters

Developing sector-specific innovation clusters that coordinate public research, private

investment, and civil society actors. The framework and infrastructure must be set up so industries

can achieve this; regulatory alignment will be a step in the right direction.

Feedback Mechanisms for Responsive Policy

Embedding feedback mechanisms to ensure that innovation policy is responsive to both market

signals and public interest. More incentives exist, with private companies leading the charge and

driving the cluster forward.

Academic Grants for Translational Institutions

Creating academic grants tailored towards supporting translational institutions that help bridge

the gap between basic research and applied, market-ready solutions.

Moreover, some policy tools commonly used to incentivize innovation, such as patent boxes have had mixed results. While effective in rewarding intellectual property ownership, these measures often benefit established firms with advanced legal and R&D capabilities without necessarily fostering inclusive or collaborative innovation ecosystems. As such, they may be better positioned as complementary to—rather than replacements for—more holistic and participatory models of innovation governance.

International Models of Triple Helix and Cluster Implementation

Several jurisdictions have developed mature Triple Helix systems that can serve as models for Canada. Their experience demonstrates that innovation thrives when institutional collaboration is formalized, targeted, and supported by strategic coordination. The goal is not necessarily to follow the exact formula implemented by our global peers but to focus on creating a system that allows us to increase our productivity as a nation.

Germany: Applied Research Through Fraunhofer Institutes

Germany’s Fraunhofer Institutes represent a globally respected applied research model that directly serves the industry’s needs. Funded through a combination of public and private sources, the institutes work closely with small and medium-sized enterprises (SMEs) to develop new technologies, prototypes, and industrial applications. This model has contributed significantly to Germany’s global leadership in high-value manufacturing and engineering innovation [1].

Denmark: Global Co-Innovation via Innovation Centres

(Image: University of Copenhagen Botanical Garden)

Denmark supports a network of Innovation Centres that facilitate collaboration between Danish universities, startups, and global partners. These centres function as soft landing zones for international co-innovation, allowing Danish companies to access global research networks while exporting domestic expertise in fields such as renewable energy, biotechnology, and health technology [2].

Singapore: State-Led Innovation Coordination

Singapore’s innovation system is built on high levels of state coordination, with government agencies such as A*STAR (Agency for Science, Technology and Research) playing a central role. These agencies actively broker partnerships between universities, multinational corporations, and startups, ensuring alignment between national priorities and research agendas. This structure has supported Singapore’s leadership in urban innovation, health technology, and industrial R&D [3].

Canada’s Current Landscape and Opportunities for Reform

The goal is not merely to increase funding but to align incentives and clarify roles within the innovation ecosystem. The Triple Helix model provides a practical framework for doing so, with the potential to deliver more coherent and outcomes-focused innovation strategies. Compared to Germany, Denmark, and Singapore, Canada’s approach to innovation collaboration tends to be broader in scope but less structured and less targeted. While existing programs aim to balance regional equity, academic excellence, and economic competitiveness, this wide mandate can dilute impact.

Canada’s innovation programs are less focused and structured than those of some other countries, which can lessen their impact. To improve outcomes, Canada should create mission-based innovation clusters, fund applied research centres focused on commercialization, prioritize long-term partnerships, modernize public procurement, and establish common evaluation frameworks.

Conclusion: Innovation as Infrastructure

Innovation should not be treated as a discrete policy area. It is foundational infrastructure, essential for economic competitiveness, public health, environmental resilience, and inclusive growth. The Triple Helix model, when effectively implemented, provides the institutional scaffolding needed to build a more coordinated, adaptive, and forward-facing innovation system. Canada has the intellectual capital, research depth, and policy imagination to realize this vision. By deepening collaboration across sectors and investing in shared platforms for innovation, the country can transform its existing strengths into a sustainable, system-wide advantage.

Sources

#InnovationCanada #TripleHelixModel #PublicPrivatePartnerships #RDIncentives #InnovationStrategy #CheckpointResearch #CanadianBusiness #ResearchAndDevelopment #EconomicGrowth #PolicyInnovation

At Checkpoint Research, we work with businesses that are pushing boundaries—whether through cross-sector collaboration, process innovation, or applied research. If your company is working with universities, developing tech-driven solutions, or simply solving tough problems in a smarter way, you might be leaving R&D funding on the table.

Let’s explore how your innovation ecosystem could be fuelling future growth.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

A quick overview

- Canada trails behind global peers in private-sector R&D investment, despite strong public research funding.

- Adopting a Patent Box tax regime (lower tax on IP-related profits) could boost private-sector innovation and IP retention.

- Countries like the UK, Turkey, and South Korea use Patent Boxes or similar policies to attract investment and drive innovation.

- OECD’s “nexus approach” ensures Patent Boxes incentivize genuine domestic R&D, not tax avoidance.

- A Canadian Patent Box aligns with global best practices, boosting competitiveness and innovation-driven economic growth.

- Canada faces a strategic choice to adopt innovation-friendly policies to stay globally competitive.

Introduction

When Canada is placed amongst its peers regarding Research & Development (R&D), one clear takeaway is the need for private-sector investment. R&D fuels economic growth, cutting-edge tech, and global competitiveness. Governments may fund the groundwork, but it’s the private sector that transforms ideas into real-world innovations that drive industries forward.

Patent Box: A Strategic Incentive for Innovation

Research and development (R&D) is a catalyst for economic growth, innovation, productivity enhancement, and global competitiveness. Countries and businesses that prioritize R&D endeavors tend to experience higher GDP growth, increased productivity, and job creation, particularly within high-skill sectors (OECD, 2023). Additionally, a robust R&D ecosystem attracts foreign investment and fosters long-term sustainability. Empirical research indicates that a 1% increase in R&D expenditure can boost GDP by 0.6% to 1.2% (Statista, 2023), demonstrating that innovation is a key driver of sustained economic success. This article explores how Canada’s R&D investment compares to leading economies like the U.S., Japan, France, Italy, the UK, Germany, and Australia. We can identify Canada’s strengths, weaknesses, and potential strategies to enhance its global innovation standing by examining these comparisons.

Canada, R&D and Patent Boxes

Canada invests heavily in public-sector research, with universities and government-backed initiatives playing a major role in advancing technology and scientific discovery. But when it comes to private-sector R&D investment, Canada lags behind global leaders like the U.S., Germany, and Japan. While other nations have developed policies that actively incentivize businesses to retain and commercialize their innovations domestically, Canada lacks a competitive tax framework to do the same.

A Patent Box system could provide that missing piece. By reducing the corporate tax rate on profits from patented technologies, businesses would have a strong incentive to develop new ideas and keep them within Canada rather than shifting their IP abroad. This could increase private R&D investment, create high-value jobs, and strengthen Canada’s position as a global innovation hub.

How Do Canada’s R&D Policies Stack Up Globally?

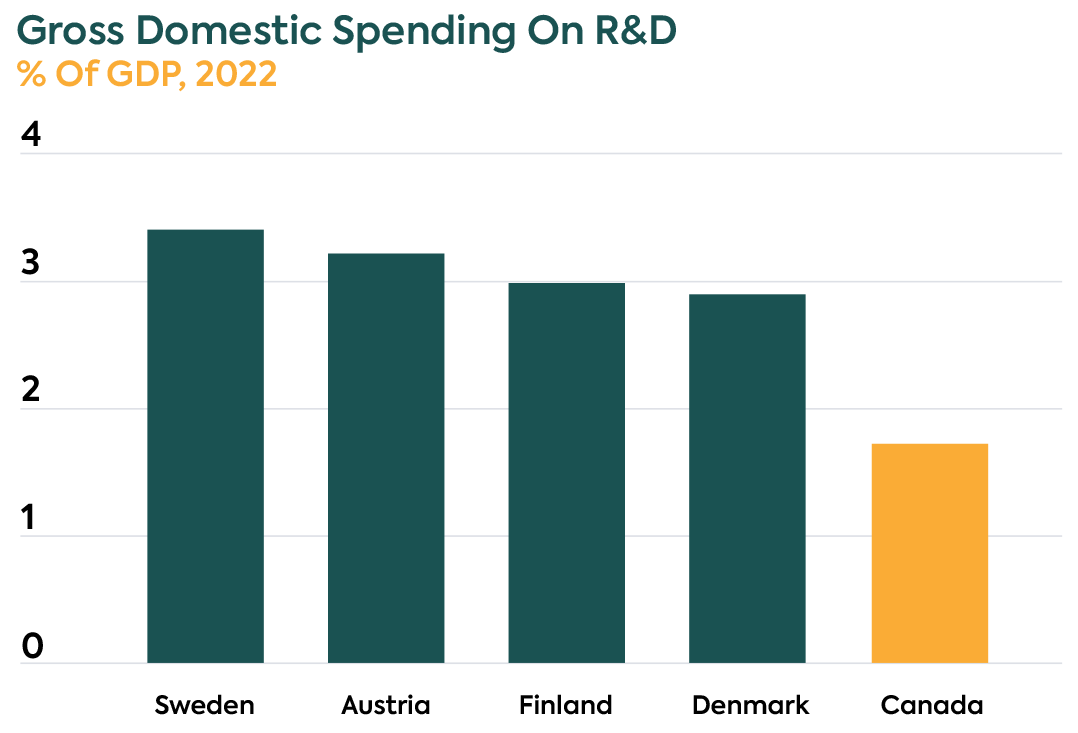

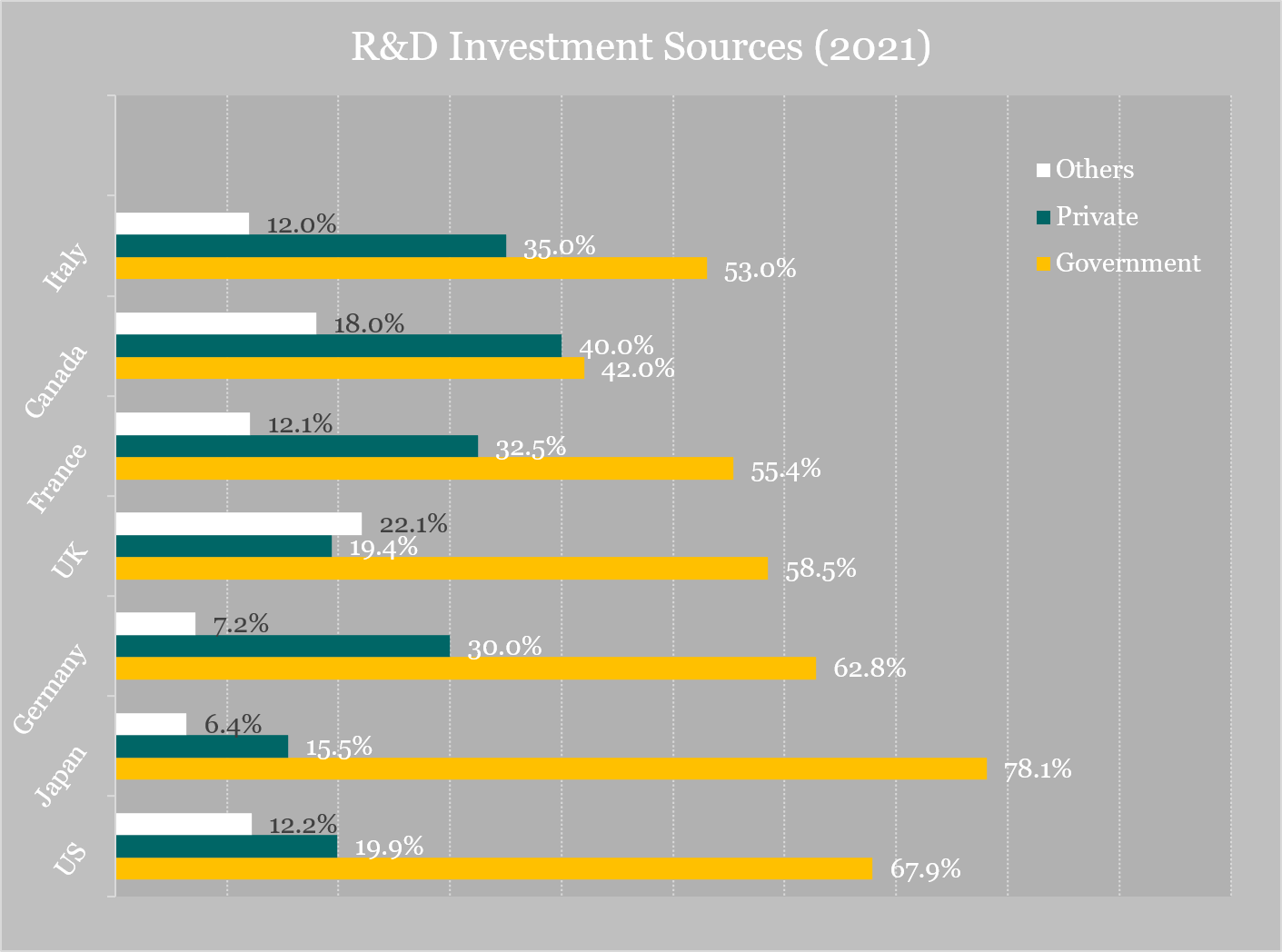

Canada’s R&D policy framework shares similarities with countries like Finland, Denmark, Australia, Sweden, and Austria, especially in its reliance on public funding, tax incentives, and strong academic institutions. However, while Canada invests 1.81% of GDP in R&D, with only 56% coming from the private sector (StatCan, 2023), these peer nations often outperform by better aligning their policies with private-sector outcomes.

For example, Finland and Denmark invest over 2.7% of GDP, driven largely by private enterprise (OECD, 2023). Both countries have strong public-private integration and innovation strategies tailored to emerging tech and green industries. Australia, despite similar structural challenges, has adopted more targeted, sector-specific innovation models. Meanwhile, Sweden leads with 3.4% R&D intensity and a risk-tolerant innovation culture, while Austria excels at balancing grants and credits to support both large firms and SMEs (OECD, 2023; Tax Foundation, 2024).

(Source: https://www.oecd.org/)

These countries demonstrate that Canada’s R&D structure isn’t inherently flawed—it’s just under-leveraged. The key difference lies in execution: more aggressive private-sector engagement, streamlined commercialization strategies, and clearer alignment between government funding and industrial growth priorities.

Patent Box Success Stories: Countries Leading the Charge

Several countries have successfully used Patent Box regimes to transform their economies into innovation hubs, attracting businesses that thrive on R&D. These policies aren’t just tax breaks; they’re strategic levers to drive cutting-edge investment, keep IP local, and foster long-term economic growth.

United Kingdom: A Global Leader in R&D Tax Breaks

The UK was one of the first to introduce a Patent Box, offering a 10% corporate tax rate on profits from qualifying patents (gov.uk). The results? Companies like GlaxoSmithKline and Arm Holdings have stayed put, taking full advantage of the incentive. The tech and pharma sectors in particular, have flourished, proving that when R&D becomes more profitable, businesses double down.

The UK’s approach to innovation extends beyond tax breaks. The government also invests in initiatives such as R&D grants, innovation accelerators, and tech incubators to further stimulate high-growth industries. This multi-pronged strategy has positioned the UK as a dominant force in the global innovation landscape.

Turkey: The Underdog Making Big Moves

Turkey is positioning itself as a major innovation hub. Their approach? Zero corporate tax on revenue from patents and utility models registered in Turkey (wipo.int). Alongside massive R&D tax deductions, this makes Turkey increasingly attractive for startups and tech firms. With its booming defense, fintech, and AI sectors, Turkey is proving that a well-structured Patent Box can be a game-changer.

Additionally, Turkey has launched initiatives like Techno-Parks and research clusters to create an ecosystem where businesses, universities, and research institutions collaborate to drive technological progress. This ecosystem has been instrumental in Turkey’s rapid rise as a technology-driven economy.

South Korea: The Tech Powerhouse Playing It Smart

Daejeon, the technology and research capital of South Korea.

While South Korea does not operate a traditional Patent Box regime, it offers various tax incentives to promote research and development (R&D) and the commercialization of intellectual property (IP). These measures include tax credits for R&D expenditures and tax exemptions for income derived from the transfer or lease of patents. Such incentives encourage companies like Samsung, LG, and Hyundai to reinvest in next-generation technologies, thereby maintaining South Korea’s competitive edge in sectors like technology, AI, and semiconductors.

The government’s commitment to technological advancement, combined with an innovation-friendly tax environment, has solidified South Korea’s status as a tech superpower. By providing tax benefits linked to patent-driven profits, South Korea effectively encourages domestic innovation and the retention of IP within the country. (Worldwide Tax Summaries Online)

Other Global Leaders in Patent Box Success

Beyond these three, several countries have seen massive success with Patent Box regimes:

Netherlands: The 9% “Innovation Box” tax rate keeps clean energy and software industries thriving (en.wikipedia.org).

Ireland: The 6.25% Knowledge Development Box has attracted giants like Google and Pfizer, making the country a major research hub (irishtimes.com).

France, Belgium, Spain, Italy: These nations have fine-tuned their Patent Box policies to retain high-value industries and prevent tax avoidance.

The OECD’s Role in Regulating Patent Boxes

While Patent Boxes effectively drive innovation, they’ve also been scrutinized by the Organisation for Economic Co-operation and Development (OECD). The Base Erosion and Profit Shifting (BEPS) initiative raised concerns that companies were using these regimes as tax loopholes rather than genuine R&D incentives (oecd.org).

To counteract this, the OECD’s BEPS Action 5 introduced the nexus approach, ensuring that tax benefits directly correlate with R&D conducted in the country offering the incentive. This prevents multinationals from simply relocating their IP to low-tax jurisdictions without conducting real R&D. Countries like the UK, Netherlands, and Ireland have since adjusted their Patent Box schemes to comply with these global standards, ensuring they support true domestic innovation rather than tax avoidance.

The Bigger Picture: Why Patent Boxes Matter

Patent Boxes aren’t just tax breaks—they’re strategic power moves. They give businesses a financial incentive to invest in innovation rather than shifting profits offshore. Countries that get this right don’t just attract businesses—they keep them.

Governments worldwide are leveraging Patent Boxes and similar tax incentives to keep innovation local and give businesses an edge in R&D. The UK’s Patent Box offers reduced tax rates on qualifying IP income, while Belgium, Portugal, and Luxembourg provide up to 85% tax deductions on innovation-related earnings. Ireland’s Knowledge Development Box (6.25%) and Poland’s ultra-low 5% IP tax rate highlight just how competitive these regimes have become. Even China, Israel, and South Korea have implemented similar high-tech IP tax breaks to fuel homegrown innovation. From France and Spain to Hungary and Switzerland, these tax-friendly policies are proving to be key drivers of economic growth, tech leadership, and private-sector R&D investment. (Source: Tax Foundation)

Lowering tax rates on IP-driven earnings creates a ripple effect:

Increased private-sector R&D investment

Higher job creation in tech and STEM fields

Stronger global competitiveness

A steady stream of new, homegrown innovations

Conclusion: The Race for Innovation

With our peers implementing innovation-friendly tax policies, Canada faces a key decision on how to support research and development. As global competition in this space grows, establishing a Patent Box framework could be an opportunity to enhance Canada’s innovation landscape and remain competitive in attracting investment. The question is whether Canada will take this step to align with international trends.

Sources

- UK Patent Box Regime – gov.uk

- Turkey’s Patent Box Regime – WIPO

- Netherlands’ Innovation Box – Wikipedia

- Ireland’s Knowledge Development Box – Irish Times

- OECD BEPS Action 5 – Nexus Approach

- Patent Box Regimes in Europe – Tax Foundation

- UK Patent Box Deduction Formula – gov.uk

- OECD Secretary-General Report to G20 Finance Ministers

- https://taxsummaries.pwc.com/republic-of-korea/corporate/tax-credits-and-incentives

#Innovation #Technology #Entrepreneurship #CanadaBusiness #R&DInvestment #PatentBox #TechPolicy #EconomicDevelopment #IntellectualProperty #GlobalCompetitiveness

Investing in research and development is essential for driving innovation, boosting economic growth, and keeping Canada competitive on the global stage. With the right policies, incentives, and private-sector commitment, Canada can close the R&D gap and strengthen its position in key industries.

If you're looking to optimize your R&D strategy, secure funding, or navigate innovation incentives, our team is here to help. Contact us today to explore how strategic R&D investments can accelerate your business growth.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

Contents

A quick overview

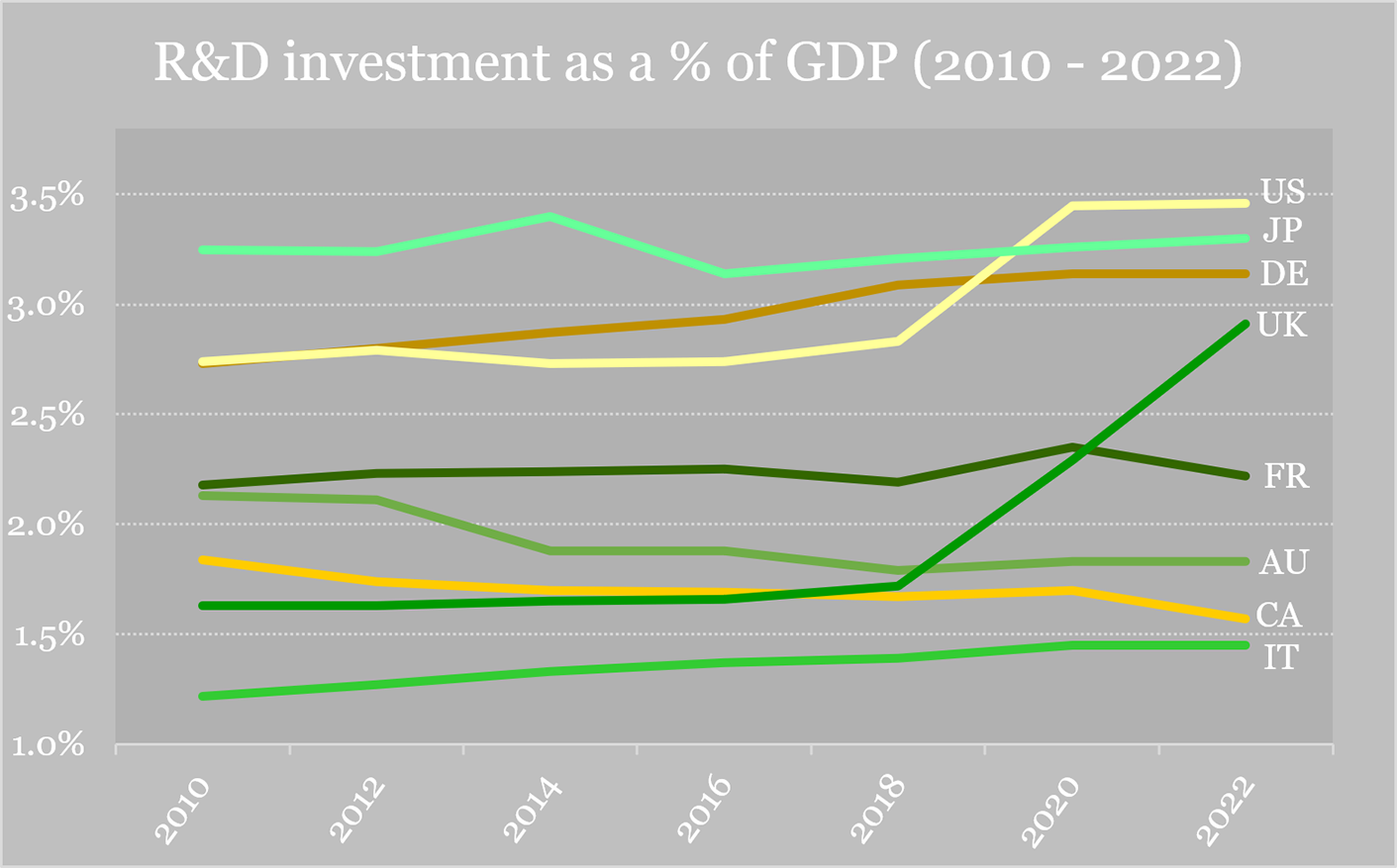

- Canada’s R&D spending is declining – Dropping from 1.87% of GDP in 2021 to 1.81% in 2022, falling behind G7 and OECD averages.

- Private-sector investment is weak – Unlike U.S. (73%) and Japan (70%), Canada struggles to drive business-led R&D.

- Global competitors are advancing faster – Germany (3.1%), Japan (3.7%), and the U.S. (2.5%) continue to increase R&D investment.

- Successful policies elsewhere offer lessons – The U.S., France, and UK use strong tax credits and funding programs to boost innovation.

- Canada must act to stay competitive – Better incentives, private-sector investment, and policy shifts are needed to close the gap.

- Strategic reforms are key – Aligning with global leaders and focusing on high-tech industries can fuel long-term growth.

Introduction

Canada has long been recognized for its innovation and research potential, yet its R&D investment is falling behind global competitors. While countries like Germany, Japan, and the U.S. continue to ramp up funding and incentives, Canada’s R&D spending has declined as a percentage of GDP, raising concerns about long-term competitiveness. Without stronger private-sector investment and better tax incentives, Canada risks lagging in key industries like technology, healthcare, and advanced manufacturing.

So, how does Canada compare to global leaders in R&D? And what steps can be taken to bridge the gap? This article explores Canada’s current R&D landscape, international best practices, and strategies to strengthen innovation.

Research and Development (R&D): A Catalyst for Economic Growth

Research and development (R&D) is a catalyst for economic growth, innovation, productivity enhancement, and global competitiveness. Countries and businesses that prioritize R&D endeavors tend to experience higher GDP growth, increased productivity, and job creation, particularly within high-skill sectors (OECD, 2023). Additionally, a robust R&D ecosystem attracts foreign investment and fosters long-term sustainability. Empirical research indicates that a 1% increase in R&D expenditure can boost GDP by 0.6% to 1.2% (Statista, 2023), demonstrating that innovation is a key driver of sustained economic success. This article explores how Canada’s R&D investment compares to leading economies like the U.S., Japan, France, Italy, the UK, Germany, and Australia. We can identify Canada’s strengths, weaknesses, and potential strategies to enhance its global innovation standing by examining these comparisons.

Canada's R&D Investments

Canada’s R&D investments span multiple key sectors, driving innovation and economic growth. In 2022, the business enterprise sector led the way, contributing approximately $19 billion, followed by the federal government allocating $8.25 billion toward national research initiatives (Statista, 2023). The higher education sector, including universities and colleges, invested $7.5 billion, fostering academic advancements. Additionally, foreign entities contributed $3 billion, reflecting Canada’s strong global research partnerships. Provincial governments also played a role, investing $1.5 billion in regional innovation, while private non-profits injected $500 million into various research projects. These combined efforts underscore Canada’s commitment to R&D, ensuring continued scientific, technological, and industry progress.

However, according to Statistique Canada, Canada’s dedication to innovation—measured by R&D expenditure as a percentage of GDP—declined from 1.87% in 2021 to 1.81% in 2022 (StatCan, 2023). This places Canada behind the G7 average and even further behind the OECD average. This decline is significant, especially as major competitors like the U.S. and Japan increased their R&D investments during the same period. The primary reason for this downturn is a lack of private sector investment, which hinders Canada’s ability to compete globally in sectors such as technology, healthcare, and advanced manufacturing (OECD, 2023).

How Do Other Countries Leverage R&D for Economic Growth?

(World Bank Data & other sources)

United States' R&D Investments

The United States maintains its global leadership in innovation through strategic federal funding, tax incentives, and forward-thinking legislation. In 2021, the U.S. invested $789 billion in R&D, with 73% originating from the private sector, representing 2.5% of GDP (National Science Foundation, 2023). The R&D Tax Credit, established in 1981 and made permanent in 2015, incentivized companies to claim $11.8 billion in tax credits in 2020 (Tax Foundation, 2023).

Landmark policies like the CHIPS and Science Act of 2022 have funneled billions into semiconductor production, AI research, and quantum technology (Wired, 2023). With a dense policy framework and strong private-sector investment, the U.S. sets the global benchmark for business-driven R&D.

France's R&D Investments

France supports business R&D through tax incentives, funding programs, and a strong innovation ecosystem. The private sector contributes nearly two-thirds of total R&D spending, with the Crédit d’Impôt Recherche (CIR) tax credit allowing companies to deduct R&D expenses from taxable income. This initiative costs the government approximately €6 billion annually (Le Monde, 2023). France’s R&D intensity is around 2.2% of GDP, but debates persist regarding the distribution of tax incentives between large corporations and SMEs.

Over 50% of CIR funding benefits large enterprises, prompting calls to redirect resources toward SMEs, as they often face greater challenges securing R&D funding despite being more agile and innovative (Le Monde, 2023).

Italy's R&D Investments

Italy has seen a transformation in R&D investment over recent years. In 2016, Italy’s gross domestic expenditure on R&D (GERD) hit €23.2 billion, marking a 4.6% increase from the previous year (OECD, 2023). However, R&D intensity was only 1.38%, below the EU average, largely due to declining investment by Italy’s largest firms. Encouragingly, SMEs have increased R&D spending, helping to stabilize the country’s overall R&D performance.

United Kingdom's R&D Investments

The UK’s business R&D sector remains a key driver of innovation, with companies investing £50 billion in 2023, led by pharmaceuticals (£8.7 billion, 17.4%) (ONS, 2023). London (£11 billion), the East of England (£9.7 billion), and the South East (£8.5 billion) were the top R&D investment regions.

While government tax incentives and grants have bolstered R&D investment, the UK’s global ranking is slipping. The number of UK companies among the top global R&D spenders has dropped from 118 in 2013 to just 63 in 2023 (FT, 2023). Meanwhile, the U.S., China, and Germany continue expanding R&D funding at a faster pace. The UK must enhance funding strategies, strengthen industry-academia collaboration, and accelerate private-sector R&D investment to remain competitive.

Germany's R&D Investments

Germany preserves a robust framework for managing business research and development (R&D), with private companies driving innovation through substantial investments. In 2022, German businesses invested approximately €82 billion in R&D, representing over two-thirds of the nation’s total R&D expenditure (Germany Trade & Invest, 2023). This reflects a consistent upward trend, with business R&D spending increasing by 8% compared to the previous year. The automotive sector plays a dominant role, with Volkswagen alone allocating nearly €19 billion to R&D efforts (Germany Trade & Invest, 2023). Overall, Germany’s R&D intensity reached 3.1% of its GDP, surpassing the European Union’s 3% target, reinforcing the country’s commitment to fostering innovation through business-led research investments (Germany Trade & Invest, 2023).

Japan's R&D Investments

Japan has a highly structured, well-funded R&D ecosystem, with businesses contributing 70% of total R&D expenditure. In 2023, Japan’s total R&D spending reached $162.2 billion, or 3.70% of GDP—one of the highest R&D intensities globally (Japan Ministry of Economy, 2023). Transportation equipment ($32.7 billion), pharmaceuticals ($11.3 billion), and electronic components ($10.1 billion) led business R&D investments.

Japan’s government prioritizes emerging technologies, investing $1.8 billion in biotech, $1.3 billion in AI, and $860.3 million in quantum research. With 14 researchers per 1,000 employees, Japan’s innovation ecosystem remains one of the world’s most advanced (Japan Science and Technology Agency, 2023).

Australia's R&D Investments

According to the Australian Bureau of Statistics, businesses invested $20.6 billion in R&D in 2021-22, a 14% increase from previous years. However, R&D spending remains at just 0.9% of GDP, well below the OECD average of 2.7% (ABS, 2023).

Australia relies on the Research and Development Tax Incentive (RDTI) to encourage business innovation, but policymakers have been hesitant to expand these incentives. Leaders like Ed Chung, CEO of TechnologyOne, argue that companies should self-fund innovation, with TechnologyOne reinvesting 25% of annual revenue into R&D (The Australian, 2023).

Where Does Canada Stand?

Canada lags behind major economies in business R&D investment, with R&D spending at just 0.9% of GDP. In comparison, Japan (3.3%), the U.S. (3.46%), France (2.22%), Italy (1.45%), and Australia (1.83%) all invest more in innovation-driven growth (OECD, 2023). Canada’s low R&D intensity reflects underinvestment in high-tech industries and a lack of strong government incentives. Unlike the U.S. and Japan, where private-sector innovation is heavily incentivized, Canada has struggled to mobilize businesses to increase R&D spending.

To remain competitive, Canada must increase R&D investment, strengthen tax incentives, and foster stronger private-sector innovation initiatives.

Conclusion

Canada’s declining R&D investment presents a critical challenge for its long-term economic growth and global competitiveness. While other leading economies continue to increase funding and foster private-sector innovation, Canada risks falling further behind. To bridge this gap, stronger incentives, increased private-sector participation, and strategic policy reforms are essential. By learning from global best practices and prioritizing high-tech industries, Canada can reclaim its position as a leader in innovation and ensure sustainable growth for the future.

(World Bank Data & other sources)

#ResearchAndDevelopment #Innovation #EconomicGrowth #Canada #Productivity #GlobalCompetitiveness

Investing in research and development is essential for driving innovation, boosting economic growth, and keeping Canada competitive on the global stage. With the right policies, incentives, and private-sector commitment, Canada can close the R&D gap and strengthen its position in key industries.

If you're looking to optimize your R&D strategy, secure funding, or navigate innovation incentives, our team is here to help. Contact us today to explore how strategic R&D investments can accelerate your business growth.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims