A quick overview

- Canada’s economy isn’t monolithic; each province and territory is powered by distinct sectors such as oil, agriculture, mining, finance, and tech.

- Nationally, services account for ~70% of GDP, but provinces like Alberta (oil) or Saskatchewan (agriculture) tell a very different story.

- Natural resources dominate in Alberta, Newfoundland & Labrador, and B.C., while mining is key in the North and parts of Quebec and Saskatchewan.

- Agriculture plays a vital role in Manitoba, Saskatchewan, and PEI, both economically and in terms of global food exports.

- Services and innovation drive Ontario, Quebec, and B.C. with sectors like finance, aerospace, AI, tourism, and tech reshaping growth.

- Emerging trends like climate transition, Indigenous-led development, and clean energy are redefining provincial roles in Canada’s economic future.

Introduction

Canada is not a monolith; it is a federation of distinct regional economies, each shaped by geography, resources, and legacy industries. From the oil sands of Alberta to the high-tech corridors of Ontario, each province and territory contributes a unique component to the nation’s broader economic architecture. To understand Canada’s economic resilience and future trajectory, we must look beyond aggregate GDP and examine the structural engines powering each region. This article offers a deep dive into the dominant economic sectors across the country, segmented by region and sector (See Figure 1).

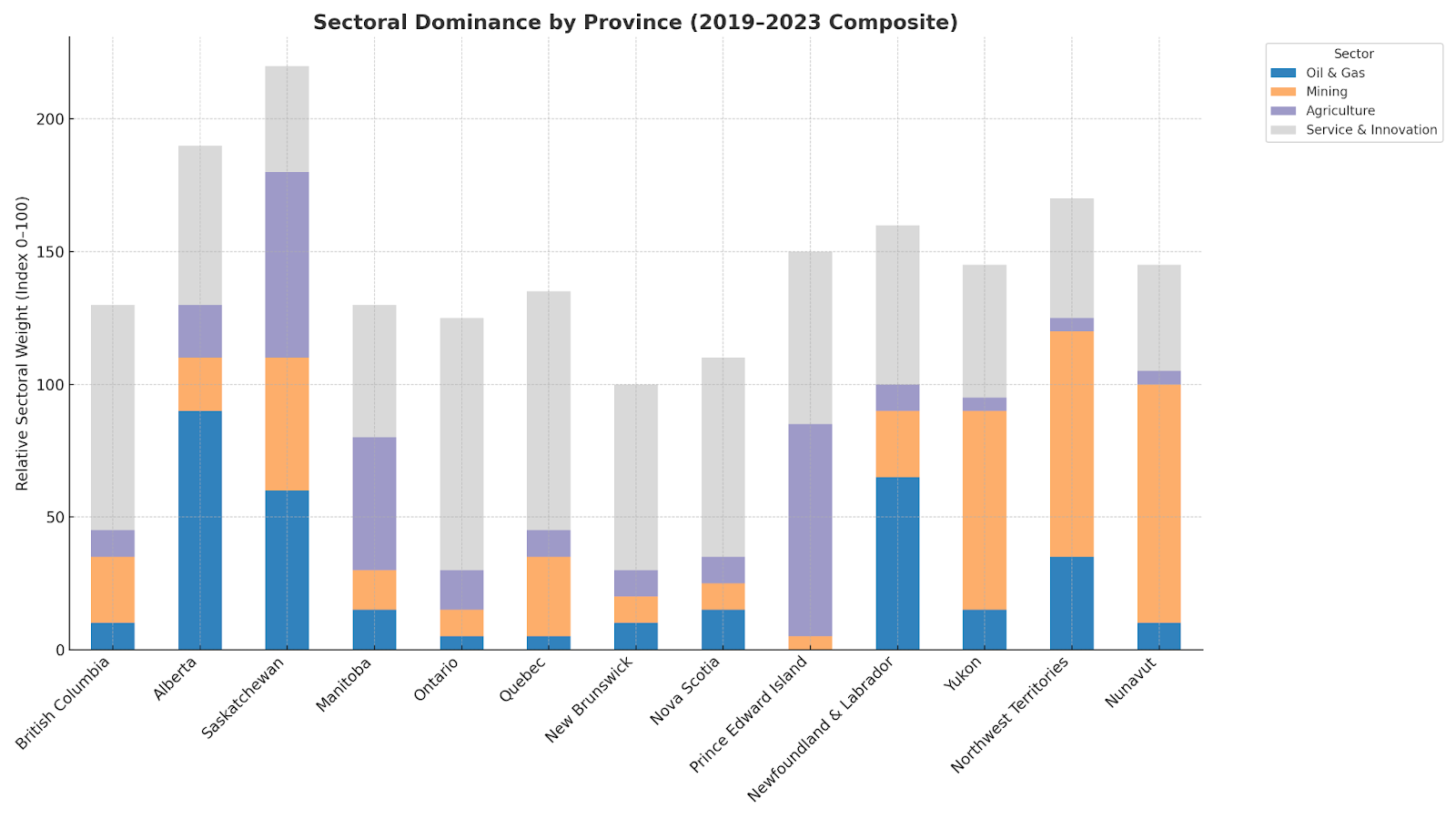

Sectoral Dominance by Province (2019–2023 Composite)

Figure 1: Sectoral dominance by province from 2019 to 2023, comparing oil & gas, mining, agriculture, and service sectors.

National Overview: The Macro Picture

As of 2023, Canada’s gross domestic product (GDP) stood at approximately $2.8 trillion CAD. The national economy is service-dominated, with the sector accounting for nearly 70% of total output. Industry, which includes manufacturing, construction, and natural resources, comprises roughly 25%, while agriculture contributes just under 2%.

Though agriculture’s share appears small, its impact is disproportionately large when measured by export value, employment in rural communities, and food sovereignty. Trade remains integral to Canada’s economic strategy, with the United States absorbing over 75% of exports. China, the European Union, and Mexico also serve as critical partners. Beneath this national framework, however, lie sharp regional distinctions that define Canada’s economic landscape.

Oil, Gas, and Hydropower: The Natural Resource Titans

Alberta

Alberta remains the epicenter of Canada’s hydrocarbon economy (See Figure 2). Oil and gas accounted for nearly 25% of the province’s GDP in 2023, with the oil sands being a cornerstone of the global energy supply.

Newfoundland & Labrador

Offshore oil extraction, particularly in the Jeanne d’Arc Basin,drives a large share of economic activity. However, the province’s dependency on global oil markets renders its economy vulnerable to price volatility.

British Columbia

BC presents a more diversified resource profile, balancing LNG exports, large-scale hydroelectric power through BC Hydro, and an enduring forestry sector.

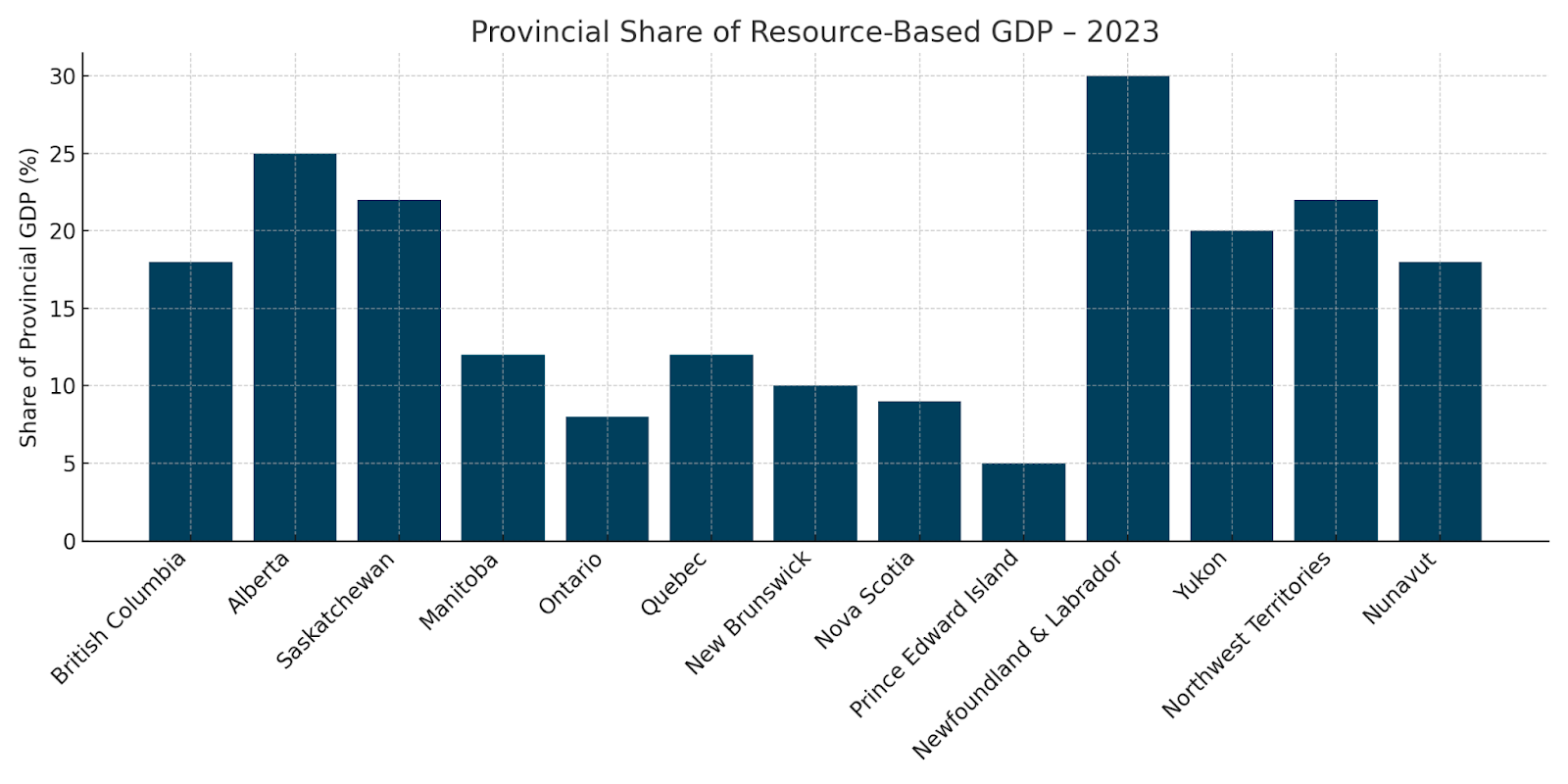

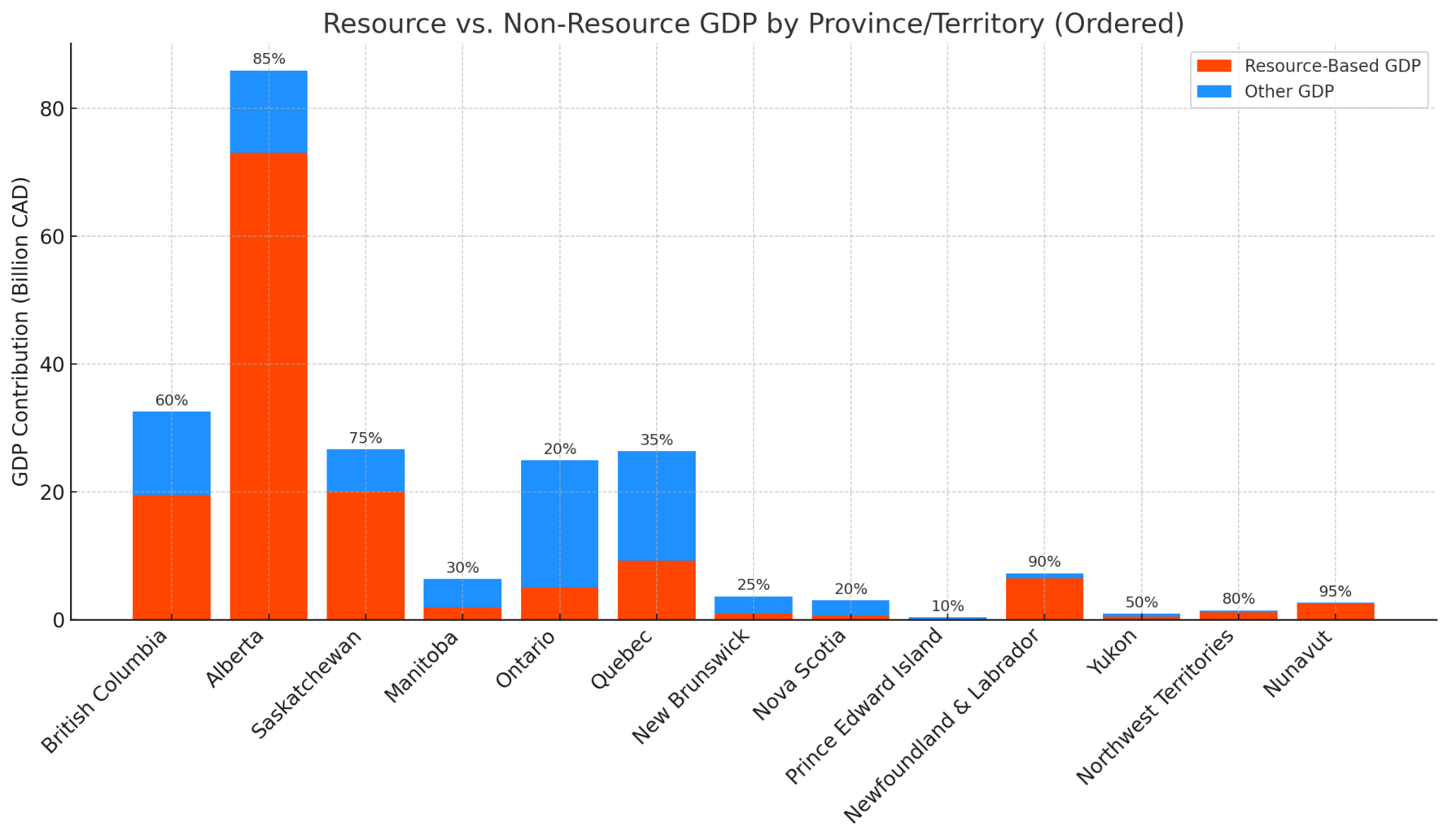

Provincial Share of Resource-Based GDP – 2023

Figure 2: Share of each province’s GDP from resource-based industries in 2023.

Mining & Minerals: The Extractive Economy

Saskatchewan

A global leader in potash and uranium production. These sectors not only underpin provincial revenues but also support global agricultural and energy systems.

Yukon, Northwest Territories, Nunavut

The northern territories are mineral-rich, with high-value outputs in gold, diamonds, and rare earth elements. These industries represent the backbone of territorial economies, often accounting for over half of GDP.

Quebec

Quebec’s mining sector is pivoting toward critical minerals- nickel, lithium, and cobalt, essential for electric vehicle batteries and renewable energy storage.

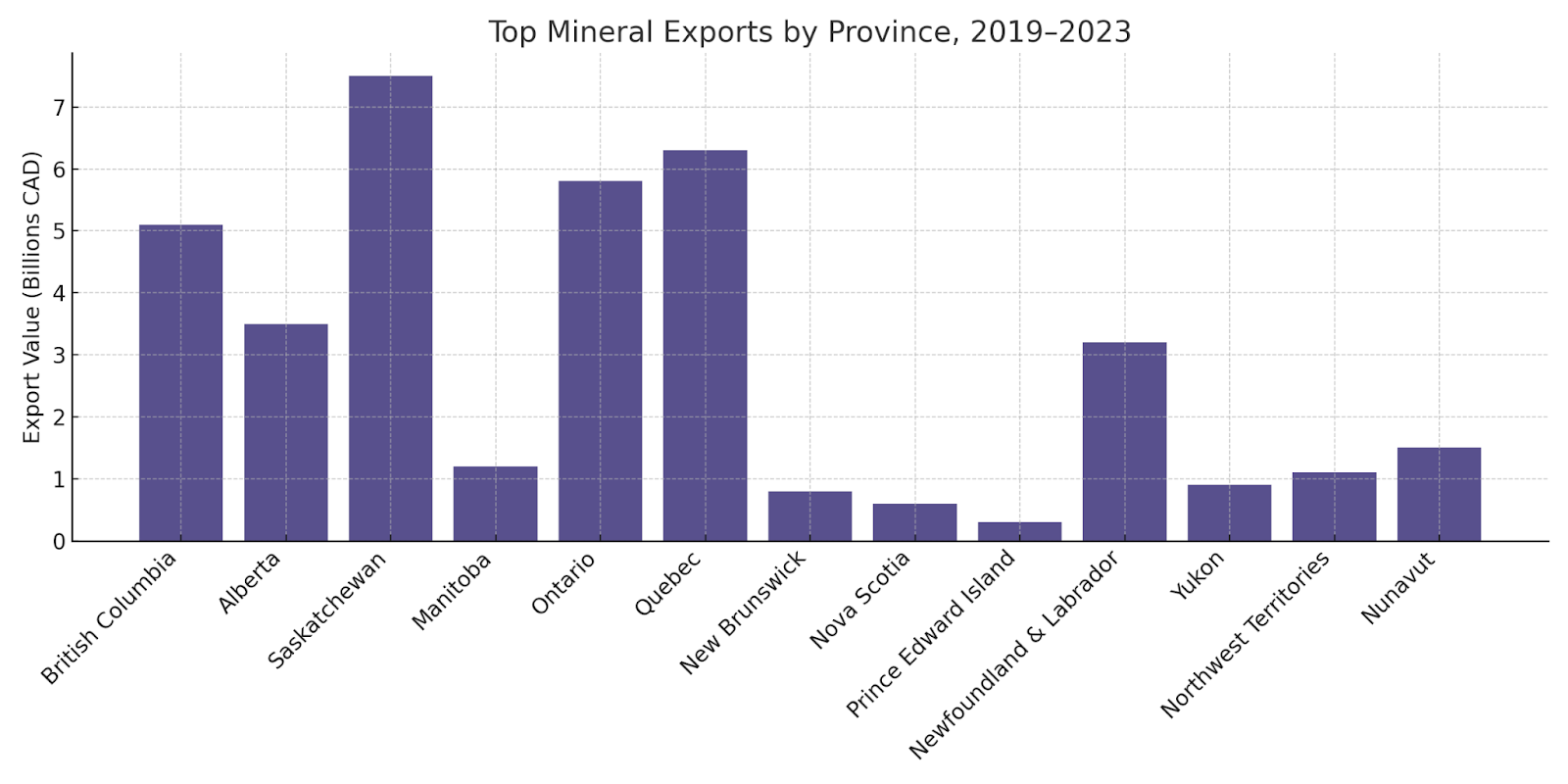

Top Mineral Exports by Province, 2019–2023

Figure 3: Leading mineral export values by province, 2019–2023 (billions CAD).

Agriculture & Agri-Tech: Sustaining Canada and the World

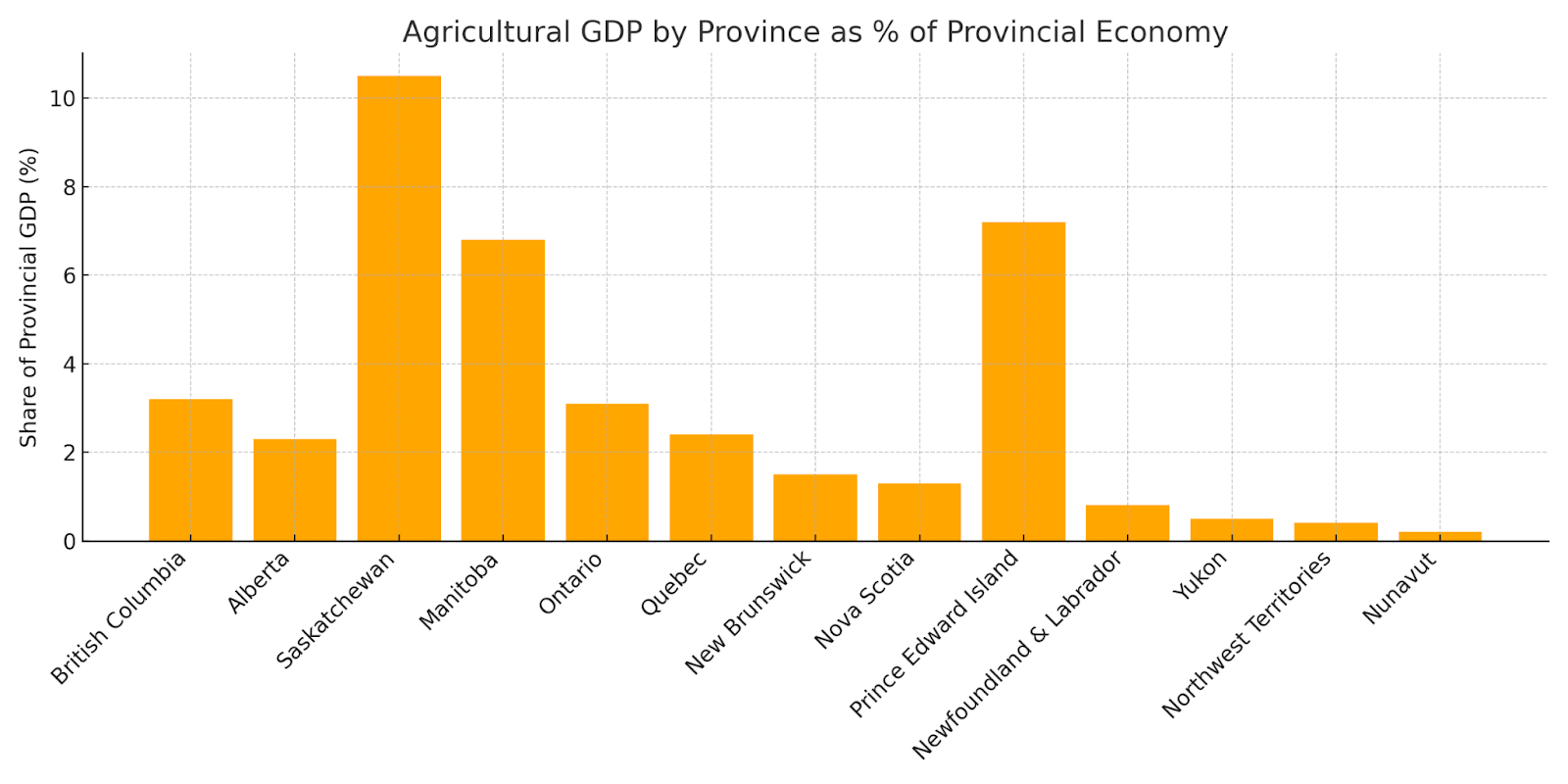

Saskatchewan

As the country’s breadbasket, Saskatchewan leads in wheat, canola, and lentils. Its agricultural exports are foundational to global food supply chains (See Figure 4).

Manitoba

A leader in hog farming, potato production, and agri-processing. Manitoba also invests significantly in agri-tech and water-efficient farming practices.

Prince Edward Island

Agriculture, particularly potatoes, dominates the island’s economy. PEI continues to modernize through crop rotation research and value-added processing.

Agricultural GDP by Province as % of Provincial Economy

Figure 4: Agriculture as a share of each province’s GDP; highlights regional concentration of farming output.

The Service & Innovation Economies: Engines of the Future

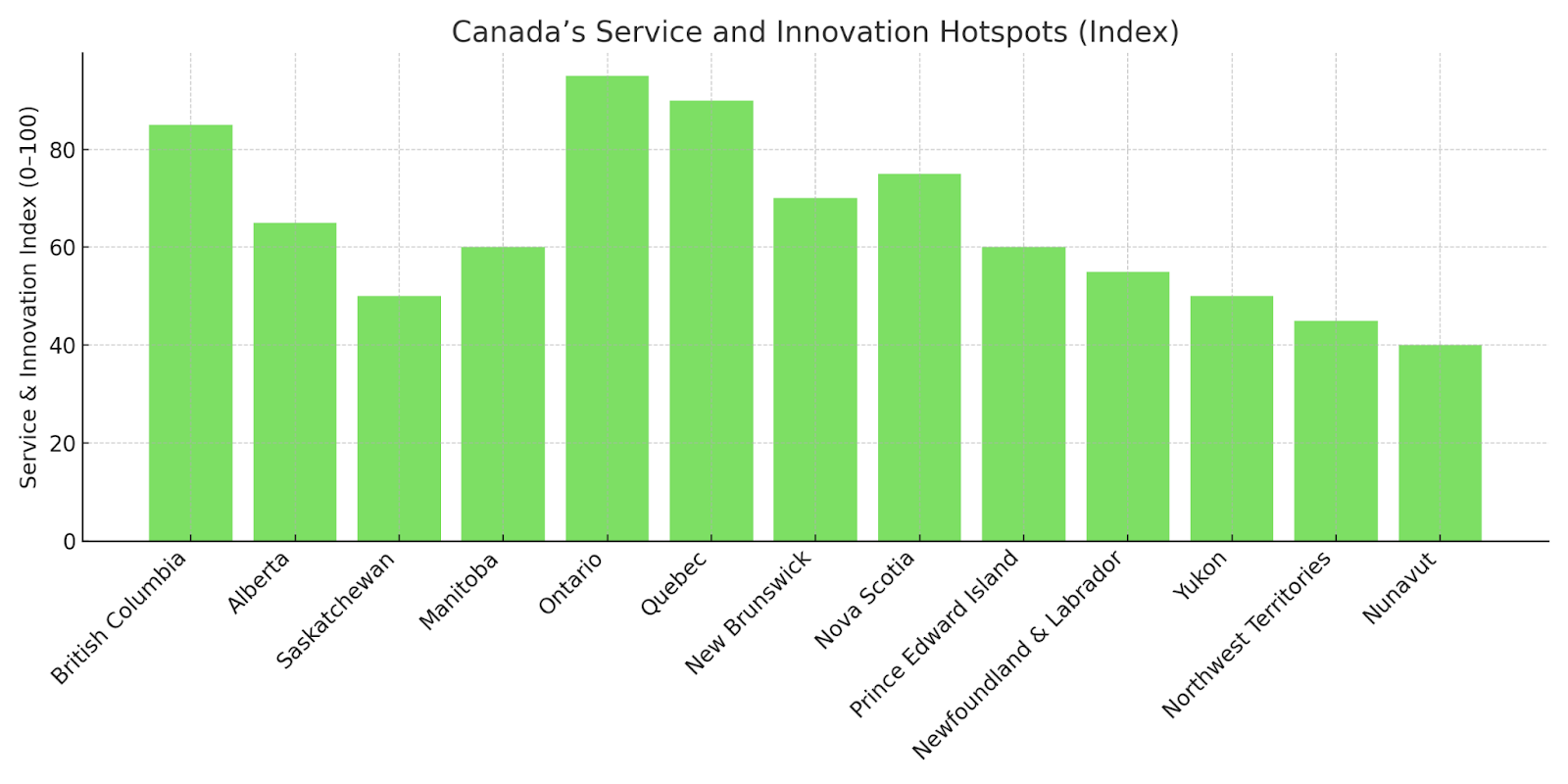

Ontario

Home to the country’s financial, technological, and manufacturing hubs. The FIRE sectors (finance, insurance, real estate) drive a substantial share of national GDP.

Quebec

Anchored by aerospace, pharmaceuticals, and AI research. Institutions like MILA and Université de Montréal position Quebec as a global AI leader.

British Columbia

Film production, tourism, and tech startups are central to BC’s growth. Vancouver increasingly competes with Seattle and San Francisco in tech innovation.

Nova Scotia & New Brunswick

With aging populations, these provinces are diversifying into marine logistics, post-secondary education exports, and renewables, with some success.

Canada’s Service and Innovation Hotspots

Figure 5: Service & Innovation Index by province; identifies Canada’s leading knowledge-economy hubs.

Territorial Economies: Resource-Rich and Logistically Challenged

- Though they contribute a small portion of the national GDP, the territories are rich in critical resources. Limited infrastructure and harsh climates remain barriers to development.

- Nunavut and the Northwest Territories rely heavily on mining, while Yukon explores diversified sectors, including ecotourism and digital entrepreneurship.

Intersections and Transitions: Trends Reshaping the Landscape

- Climate Transition: Carbon-intensive economies like Alberta and Saskatchewan must pivot and are investing in carbon capture and clean hydrogen.

- Interprovincial Migration: A tech-oriented workforce is clustering in Ontario and British Columbia, leading to demographic and economic shifts.

- Indigenous Economic Development: Indigenous communities are asserting leadership through co-ownership of resource projects and land stewardship models.

Conclusion: Strength in Complexity

Canada’s economic identity is not singular-it is a complex interplay of regional sectors, each bringing distinct strengths and vulnerabilities. From Alberta’s oil rigs to Ontario’s fintech towers and Nunavut’s mineral veins, this country’s prosperity depends on recognizing and integrating these diverse engines of growth.

To lead in an era defined by climate urgency, technological disruption, and geopolitical uncertainty, Canada must double down on regional strengths while supporting national cohesion. The future won’t be driven by one sector or one province; it will be orchestrated by many, moving in concert.

Sources

- UK Patent Box Regime – gov.uk

- Turkey’s Patent Box Regime – WIPO

- Netherlands’ Innovation Box – Wikipedia

- Ireland’s Knowledge Development Box – Irish Times

- OECD BEPS Action 5 – Nexus Approach

- Patent Box Regimes in Europe – Tax Foundation

- UK Patent Box Deduction Formula – gov.uk

- OECD Secretary-General Report to G20 Finance Ministers

- https://taxsummaries.pwc.com/republic-of-korea/corporate/tax-credits-and-incentives

#CanadianEconomy #EconomicDevelopment #ProvincialEconomies #NaturalResourcesCanada #InnovationInIndustry #AgricultureCanada #MiningCanada #CleanTechCanada #SRandED #CheckpointResearch #FutureOfWorkCanada

Canada’s economic strength doesn’t come from one sector, or even one region. It comes from the interplay of many specialized economies, each building on local expertise, natural advantages, and forward-looking strategies.

At Checkpoint Research, we help businesses across Canada’s diverse industries identify the innovation embedded in their everyday work. Whether it’s agri-tech in the Prairies, clean energy projects in B.C., or advanced manufacturing in Ontario, we translate sectoral progress into SR&ED claims that reflect the real value being created.

If your company is evolving, adapting, or modernizing within your field, let’s make sure your growth is backed by the support it deserves.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

A quick overview

- Natural resource sectors contributed 9–12% of Canada’s GDP between 2019 and 2023, generating over $250 billion annually in direct output.

- Oil & gas remained the largest contributor, peaking at $130.2B in 2022, with Alberta leading production.

- Mining & quarrying grew steadily, reaching $48.9B in 2023, driven by demand for critical minerals like lithium, copper, and nickel.

- Forestry & logging stayed stable, though dipped slightly in 2023 due to reduced construction activity.

- Hydroelectric power delivered consistent GDP contributions (~$30B/year), with Quebec, BC, and Manitoba as primary producers.

- Provincial economies vary widely: Alberta dominates in oil, Quebec in hydro, BC in forestry, and Ontario in mining.

Introduction

Canada’s economic landscape has been forged by the geography it inhabits. Beneath its surface lie commodities that have historically propelled growth, attracted foreign capital, and positioned the nation as a global resource heavyweight. But what do the hard numbers tell us about the real contribution of oil, minerals, forests, and hydroelectric power over the past five years? And how are these assets distributed across provinces?

This article gives a glimpse of Canada’s resource economy, sector by sector, province by province—unveiling the economic weight of each natural resource and their evolution from 2019 to 2023.

Canada’s GDP and the Natural Resource Contribution

Between 2019 and 2023, Canada’s nominal GDP increased from approximately $2.0 trillion to $2.8 trillion, driven by the post-pandemic recovery, inflationary pressures, and a strong global demand for commodities. During this period, natural resource sectors consistently contributed between 9% and 12% to the country’s GDP. Oil and gas extraction alone ranged from 6.4% in 2019 to over 3% by 2023, reflecting volatility in global energy markets. Mining and quarrying (excluding oil and gas) held steady at about 1.7%, while forestry and hydroelectric power accounted for 1.2% and approximately 1.2%, respectively, underscoring the foundational role of renewable energy in Canada’s economic mix.

Together, these sectors generated over CAD 250 billion annually in direct economic output, not including the substantial ripple effects across manufacturing, logistics, and services. The economic footprint of each resource varies widely by province—Alberta dominates in oil and gas, Quebec leads in hydroelectric power, British Columbia in forestry, and Ontario in mining, creating a geographically diverse but deeply interconnected resource economy. These sectors are more than just export engines; they are structural pillars that shape employment, investment, and regional development across Canada.

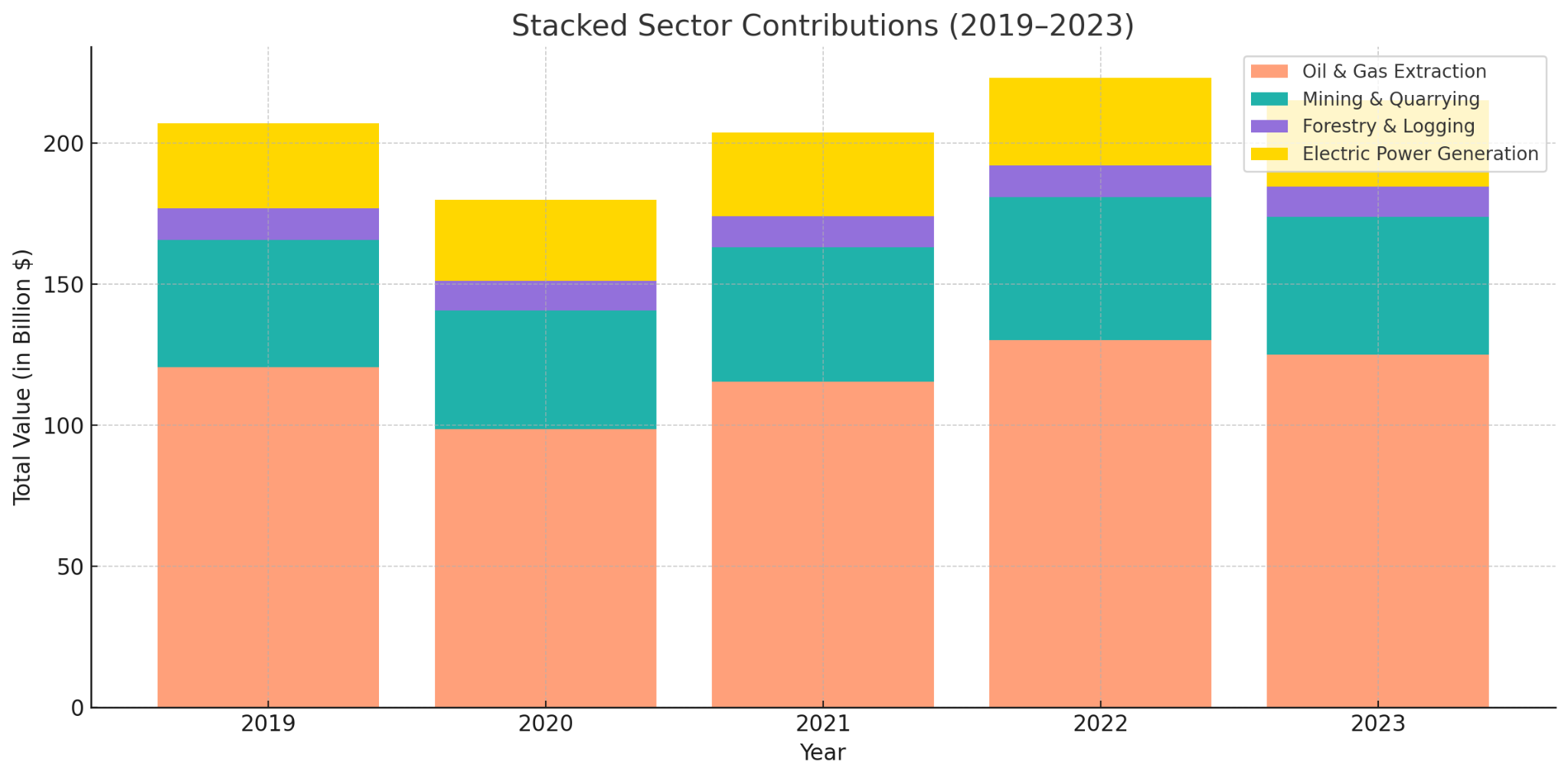

National GDP Trends by Resource Subsector

The graph below tracks the GDP contributions (in billions of CAD) from Canada’s four major natural resource sectors between 2019 and 2023:

Oil & Gas Extraction

Oil and gas has remained Canada’s largest individual contributor within the resource economy, peaking at $130.2 billion in 2022. Although 2023 showed a slight retraction to $125.0 billion, Alberta continues to dominate this sector with extensive operations in the oil sands and conventional extraction.

Mining & Quarrying

A sector increasingly influenced by global electrification, mining has expanded from $45.3 billion in 2019 to $48.9 billion in 2023. Ontario and Quebec have emerged as leaders, particularly in the extraction of gold, nickel, copper, and lithium—key components of the clean energy transition.

Forestry & Logging

Forestry remains critical to regional economies, especially in British Columbia and Quebec. GDP contributions have hovered between $10.5–11.3 billion, with a slight dip in 2023 reflecting reduced construction activity and lumber exports.

Electric Power Generation

Niagara Falls hydroelectric plant

Hydropower remains a quiet juggernaut. With GDP contributions maintaining around $30 billion annually, Quebec, BC, and Manitoba are responsible for the majority of Canada’s clean electricity output. Modest growth in renewables like solar and wind is evident, particularly in Alberta and Ontario.

Resource GDP by Region: A Provincial Breakdown

Provincial Contributions to Resource GDP

- Alberta leads the nation with nearly $86B, largely from oil and gas.

- British Columbia’s strength lies in forestry and hydro.

- Saskatchewan’s contributions stem from potash, uranium, and agri-minerals.

- Quebec and Ontario offer a mix of mining and hydroelectric generation.

- Territories and Atlantic Canada, though smaller in volume, rely heavily on resources relative to their GDP sizes.

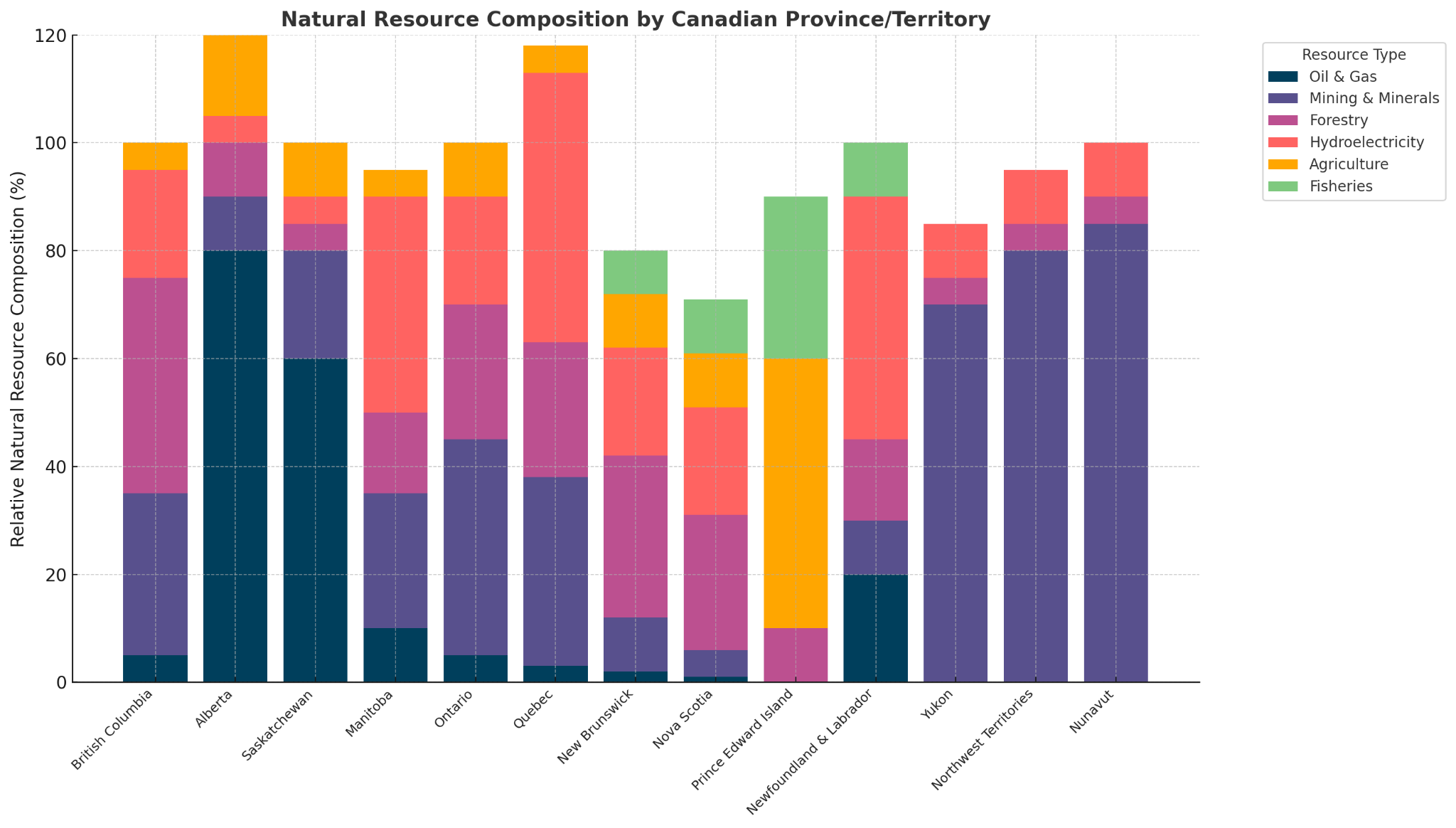

Canada’s Provincial and Territorial Resource Landscape

Canada’s provinces and territories are blessed with a kaleidoscope of natural resources, each shaping the local economy and culture. Together, these regions form a resource-rich tapestry, powering both Canada and the wider world.

Alberta – Oil, Agriculture, and Energy Exports

Alberta stands out as the titan of oil and gas, tapping into vast bitumen reserves in the Athabasca oil sands while supporting agriculture on its prairie plains.

British Columbia – Timber and Mineral Riches

British Columbia is famed for its towering forests and booming forestry industry, alongside rich deposits of copper, coal, and gold, making it a dual force in timber and mining.

Saskatchewan – Potash, Uranium, and Prairie Crops

In addition to oil and gas, Saskatchewan is a powerhouse of uranium and potash production, and a breadbasket for wheat and canola.

Quebec – Hydropower and Critical Minerals

Quebec is a hydroelectric giant, with rivers fueling a vast clean energy network. Its mineral bounty includes iron ore, gold, and emerging lithium deposits vital to green tech.

Ontario – Mining Heritage and Energy Support

Ontario boasts a deep mining history with world-class nickel, gold, and platinum group metals, while also contributing significantly to forestry and electric power generation.

Manitoba – Hydroelectric Excellence and Metal Production

Manitoba quietly excels in hydroelectric generation and is a key player in zinc and nickel mining.

Newfoundland & Labrador – Offshore Oil and Northern Hydro

The province draws energy from offshore oil fields like Hebron and Hibernia, and boasts one of the largest hydro projects in the country—Churchill Falls.

The Maritimes – Forests, Fisheries, and Agricultural Strength

Nova Scotia, New Brunswick, and Prince Edward Island rely on forestry, fisheries, and agriculture. Nova Scotia is also historically known for coal mining.

The Territories – Canada’s Northern Mineral Frontier

Nunavut and the Northwest Territories are rich in gold, diamonds, and iron. Yukon continues its gold rush legacy with modern mining developments.

Conclusion

Over the past five years, Canada’s natural resource sectors—including oil and gas extraction, mining and quarrying, forestry and logging, and electric power generation—have contributed an estimated $205.8 billion CAD annually to the national economy. Based on an average national GDP of approximately $2.2 trillion CAD (Statistics Canada, Table 36-10-0104-01), this represents around 9.4% of total economic output.

This sustained contribution highlights the steady role that natural resources continue to play in Canada’s broader economic structure. While the share of GDP from resource industries varies significantly across provinces and territories—with some regions more heavily reliant than others—the sector remains a substantial pillar of national economic performance.

These figures provide a foundation for ongoing analysis and discussion around regional economic strategy, industrial diversification, and long-term planning—particularly as Canada navigates shifts in global demand, climate priorities, and innovation opportunities.

Source List & Reference Highlights

- Statistics Canada. Natural Resources Indicators, Q4 2023

- Statistics Canada. GDP by Industry Overview, 2023

- Statistics Canada. Natural Resources Provincial Accounts, 2023

- Natural Resources Canada. 10 Key Facts on Canada’s Natural Resources

- Statistics Canada. Natural Resources Indicators, Q4 2023

- Statistics Canada. GDP by Industry Overview, 2023

- Statistics Canada. Natural Resources Provincial Accounts, 2023

- Natural Resources Canada. 10 Key Facts on Canada’s Natural Resources

- Statistics Canada. Natural Resources Provincial Accounts, 2023

#CanadaResources #EconomicData #SRandED #InnovationInIndustry #NaturalResourceEconomy #CleanEnergyCanada #ResourceStrategy #CheckpointResearch #ProvincialEconomy #IndustrialCanada #MiningToHydro

The data tells a clear story: Canada’s resource industries remain critical drivers of economic output, investment, and regional development.

At Checkpoint Research, we work with companies across these sectors—whether you’re optimizing mining operations in Ontario, modernizing hydro infrastructure in Quebec, or improving forestry logistics in B.C. What often looks like operational problem-solving on the surface is, in fact, innovation that qualifies for SR&ED.

If your team is tackling challenges in energy, extraction, or resource efficiency, you could be missing out on federal support designed to reward that progress.

Let’s turn your technical advancements into strategic funding—so you can keep building what drives Canada forward.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

Contents

A quick overview

- Canada is rapidly scaling CCUS technologies like carbon-to-value, direct air capture, and AI-driven emissions tracking as core tools for decarbonization.

- Cross-industry innovation is driving change, with aerospace, automation, and biology reshaping how oil and gas tackles emissions and efficiency.

- Advanced water and waste solutions, from closed-loop systems to circular material reuse, are redefining environmental performance in the oil sands.

- The sector is pursuing a strategic, low-carbon transition through green-powered operations, hybrid-skilled workforce training, and real-time ESG reporting.

- Indigenous-led clean energy projects are central to the transition, combining sovereignty, sustainability, and innovation.

- Canada is shifting from a resource exporter to an innovation leader, developing scalable energy technologies with global relevance.

Introduction

There is no denying the reality: oil and gas remains a foundational pillar of Canada’s energy economy. But in 2025, the conversation has matured. It is no longer simply about output — it is about outcome. It is no longer about scale — it is about sustainability, strategy, and shared accountability.

As global net-zero ambitions become non-negotiable and intersectoral convergence accelerates, Canada’s oil and gas industry is entering a deliberate, data-driven, and design-forward phase of transformation.

This is not the twilight of a sector — it is the recalibration of an entire system.

Canada’s Oil & Gas: Entering the Age of Intentional Innovation

Carbon Capture: From Concept to Cornerstone

Carbon Capture, Utilization, and Storage (CCUS) has moved from PowerPoint decks to pipeline infrastructure. It is now woven into the business models of the country’s largest producers — Cenovus, Suncor, Imperial, and beyond — and is rapidly becoming a defining marker of credibility in the global energy market.

New Frontiers in CCUS Research:

- Carbon-to-value (C2V) technologies are redefining CO₂ as a feedstock rather than a liability, with startups converting emissions into materials such as carbon nanotubes, synthetic fuels, and even concrete additives.

- Direct air capture (DAC) facilities, supported by both provincial funds and private capital (like through the Canada Growth Fund), are being tested in Alberta’s prairies, leveraging favorable geology for permanent sequestration.

- Carbon intelligence platforms — digital twins and emissions-tracking AI — are being embedded into CCUS networks to audit and optimize performance in real-time.

Canada is fast becoming a global testbed for industrial-scale decarbonization. The Oil Sands Pathways Alliance — a coalition of six of Canada’s top producers — plans to deploy one of the world’s largest CCUS networks by 2030. The future? Fully automated, modular carbon systems that not only store but dynamically reroute captured CO₂ for industrial reuse.

Cross-Industry Innovation: Where Disciplines Collide & Reconstruct

Innovation in oil and gas is no longer insular. The future is forged at the intersection, where code meets crude, satellites meet soil, and biology meets bitumen.

Aerospace & Geospatial Tech

Canadian companies are deploying space-based methane monitoring systems (like GHGSat) that offer emissions transparency down to the facility level. Some are using LIDAR-equipped drones for 3D modeling of terrain shifts, helping predict subsidence risks before they become disasters.

AI & Automation

Predictive analytics platforms are reducing equipment failures by 40%, and AI-driven subsurface modeling is eliminating trial-and-error drilling, resulting in faster timelines and smaller footprints. Natural Language Processing is even being used to parse historic drilling logs to uncover overlooked reservoirs.

Bio-Inspired Design

Research institutions are investigating biochar-based tailings remediation, harnessing agricultural byproducts to stabilize and detoxify mining waste. Fungal mycelium is also being explored for its ability to bio-sequester toxins in contaminated soils.

The energy sector is now behaving more like a tech sector: fail-fast prototyping, iterative systems testing, and interdisciplinary hiring are becoming the norm, not the exception.

Water and Waste: The Next Sustainability Battleground

Water is emerging as both a constraint and a canvas for innovation. In the oil sands, where water-intensive processes have long been an Achilles’ heel, new systems are shifting the paradigm.

A handful of black oil rich sand from Alberta Canada.

Next-Gen Water & Waste Solutions in Canada’s Energy Sector:

Closed-Loop Innovation

The Water Technology Development Centre (COSIA) is advancing closed-loop systems that aim for 90%+ water recovery, using high-efficiency nanofiltration and real-time water chemistry monitoring.

ZLD Systems

Zero-liquid discharge systems are now being tested at scale, combining thermal evaporation, crystallization, and advanced membrane tech to ensure no wastewater is released into the environment.

Solid Waste Valorization

Fly ash and tailings are being explored as inputs for geopolymer cement, which has up to 80% lower embodied carbon than Portland cement. Other programs are repurposing hydrocarbon residues into recyclable road base materials.

Waste is being redefined — not as something to minimize, but as something to metabolize. Circularity is the new benchmark.

Neutral but Pragmatic: Navigating the Complexity of Transition

Let’s be clear: oil and gas is not going away in the short term. What is fading is the license to operate without a deeply integrated climate strategy. The path forward lies in pragmatic transition — scaling down emissions while maintaining economic resilience and energy reliability.

Strategies Driving Canada’s Shift to Cleaner Energy:

Carbon-Neutral Exploration

Companies are beginning to use green hydrogen to power drilling rigs, electrify auxiliary operations, and purchase high-quality, The agenda emphasizes utilizing verified offsets derived from nature-based projects led by Indigenous communities.

Next-Gen Training Pipelines

Upskilling programs are focusing on hybrid disciplines — think petroleum engineers with coding fluency or drone operators with environmental science credentials. Universities like UCalgary and UAlberta are redesigning curricula to support future-fit energy workers.

Policy Integration

Canada’s Clean Technology Investment Tax Credit and the Net-Zero Accelerator Fund are catalyzing risk-tolerant innovation. Investor demands for operational transparency are driving a shift in ESG reporting from static PDF documents to real-time dashboards utilizing blockchain technology. Investor pressure for operational transparency is driving a change in corporate sustainability reporting. This change involves moving from static PDF documents to real-time dashboards powered by blockchain technology.

The Horizon: From Quiet Revolution to Collaborative Renaissance

What we are witnessing is not merely a sector under pressure — it’s a sector reinventing itself. Through cross-pollination, capital realignment, and a research-first mindset, Canadian oil and gas is making a bold play: not to defy transition, but to define it.

The future belongs to those willing to experiment at scale, collaborate across silos, and embrace complexity without paralysis.

If you’re building in energy, tech, academia, or finance, now is the moment to step forward. From interprovincial pilots to public-private consortia, Canada’s energy future will not be dictated from above — it will be designed together.

Talisman Energy (now part of Repsol): Pioneering Digital Strategy in the Field

Canada’s oil and gas sector is at a precipice — not of decline, but of definition. The choices made in this decade will determine whether the country remains merely a resource provider or evolves into a global innovator in sustainable industrial transformation.

This new era means:

- Energy systems will be judged by integration, not isolation.

Carbon capture, AI, bioengineering, and digital twin technologies must work in concert to be scalable and exportable. The Canadian model could become a blueprint for decarbonization in other resource-heavy nations. - Indigenous leadership will be central, not peripheral.

Many of Canada’s most forward-thinking clean energy projects — from geothermal to reforestation carbon offsets — are being led or co-led by Indigenous communities. The future lies in a just transition built on equity, sovereignty, and shared innovation. - Workforce evolution will outpace workforce replacement.

The next generation of energy workers will not just operate wells or refineries — they’ll code optimization models, fly methane-monitoring satellites, or oversee regenerative land use. Training programs will need to be agile, transdisciplinary, and deeply inclusive. - Canada’s brand will shift from barrel-counting to brainpower.

If nurtured correctly, the innovations born in Alberta, Saskatchewan, and Newfoundland today could become tomorrow’s tech exports — from modular CCUS units to AI-powered remediation platforms.

Conclusion

In sum, the question is not “Can oil and gas evolve?” It already is. The question is: Will we resource this transition at the scale and speed the moment demands? If we do, Canada could re-emerge not only as a leader in energy, but as an architect of the post-carbon industrial world.

Source List & Reference Highlights

Carbon Capture & CCUS:

Cross-Sector Innovation

Water and Waste Management

Policy, ESG, and Funding

Indigenous-Led Energy

#EnergyInnovation #OilAndGasTech #SustainableEnergy #CleanTechCanada #CanadianEnergy #RDIncentives #CheckpointResearch #InnovationCanada #CarbonCapture #NetZeroSolutions

At Checkpoint Research, we understand that innovation in oil and gas doesn’t always look like a lab experiment—it often lives in field upgrades, AI integrations, cleantech adaptations, and operational refinements.

We help organizations in complex industries like energy structure their SR&ED processes around real-world innovation—ensuring the work you’re already doing is properly captured, supported, and strategically aligned with funding opportunities.

If your team is building smarter systems, developing in-house solutions, or adapting tech in high-stakes environments, we can help you stay organized, compliant, and ready to claim.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims

A quick overview

- Canada’s interprovincial trade barriers are a self-imposed obstacle to national economic growth—driving up costs, limiting mobility, and restricting business expansion.

- Regulatory inconsistency between provinces forces businesses to comply with multiple sets of rules, raising operational costs and reducing efficiency.

- Protected industries like dairy, alcohol, and poultry face outdated restrictions that inflate consumer prices and reduce interprovincial access.

- Labour mobility remains limited, as qualified professionals and tradespeople must re-certify across provinces, worsening shortages and delays.

- Provincial infrastructure and procurement policies often prioritize local players, stifling national competition and innovation.

- Despite the Canadian Free Trade Agreement (CFTA), many provinces retain exemptions, and enforcement remains inconsistent—though progress is underway in Alberta, Manitoba, and Nova Scotia.

Introduction

With pending U.S. tariffs on the horizon, concerns about Canada’s economic future are rising. Trade restrictions come in many forms, but whether they stem from U.S. tariffs or Canada’s interprovincial trade barriers, the result is the same—higher costs, reduced business competitiveness, and unnecessary obstacles to economic growth. The key difference? One is imposed by a foreign government, while the other is self-inflicted.

Interprovincial trade barriers refer to regulatory, legal, and economic restrictions that limit the free movement of goods, services, labor, and investment between Canadian provinces and territories. These obstacles increase costs for businesses and consumers, ultimately reducing economic efficiency (RBC Thought Leadership, 2024). Despite Canada’s strong commitment to free trade on the global stage, its internal trade system remains fragmented, making it easier in some cases to do business with the U.S. or EU than between provinces.

Brief History of Interprovincial Barriers in Canada

Interprovincial trade barriers in Canada have existed since the Confederation in 1867, despite the Constitution’s intention to create a unified economic market. Section 121 of the Constitution Act promised free trade across provincial borders, but in practice, provinces imposed their own rules, regulations, and restrictions on goods, services, labor, and mobility.

Over time, these barriers have taken the form of inconsistent licensing rules, product standards, transportation regulations, and alcohol distribution laws, among others—often to protect local industries or due to regulatory patchwork. Efforts to fix this include the 1995 Agreement on Internal Trade (AIT) and its 2017 successor, the Canadian Free Trade Agreement (CFTA), designed to reduce these barriers. That said, not all differences are arbitrary; in some cases, they reflect legitimate regional concerns. A province may be better equipped to set standards for local issues like water safety, environmental protection, or resource management—areas where flexibility and local knowledge are essential.

However, enforcement remains limited, and many barriers persist, costing the Canadian economy billions in lost productivity and investment yearly (CFIB, 2022). The issue continues to spark debate over federalism, economic integration, and national competitiveness.

Breaking Down the Cost Drivers Behind Canada’s Interprovincial Trade Barriers

Regulatory Differences

One of the most persistent trade barriers is regulatory inconsistency. Each province operates under its own rules and standards, creating challenges for businesses trying to expand nationwide. A product that meets Ontario’s packaging and labeling laws may require modifications before being sold in Quebec. Likewise, differences in safety and environmental regulations force companies to comply with multiple sets of standards, increasing both costs and delays. Instead of a single, unified market, businesses must navigate a patchwork of conflicting provincial rules that slow trade and stifle economic efficiency.

Industry Protectionism and Supply Management

Wine produced in British Columbia often never reaches dinner tables in Ontario, not because of quality or demand, but due to arcane provincial trade barriers and outdated regulations. Certain sectors remain heavily regulated, operating under provincial quotas and trade restrictions that limit competition. Dairy, poultry, and alcohol are some of the most protected industries, with strict provincial controls preventing businesses from freely selling their products across Canada. The dairy industry, for instance, is bound by supply management systems that dictate production and pricing, keeping farmers locked within their provincial markets. Similarly, liquor distribution remains tightly regulated, with government-controlled monopolies restricting cross-border alcohol sales. While these measures are designed to protect local industries, they also inflate prices and limit consumer choice.

Labour Mobility

Skilled workers often face barriers to practicing in different provinces, even when their qualifications are identical. Doctors, nurses, engineers, and other regulated professionals must frequently re-certify or meet additional licensing requirements before they can work in another province. The same holds true for skilled trades, where apprenticeship programs and certification rules vary significantly across jurisdictions.

While the Red Seal Program was created to allow tradespeople—like electricians, plumbers, and heavy-duty mechanics—to work across Canada without retraining, not all provinces recognize all Red Seal trades equally, and provincial regulations can still create friction. For example, a Red Seal-certified welder in Alberta may face additional assessments before working in Quebec or Nova Scotia, adding unnecessary delays and costs. These restrictions exacerbate labor shortages, making it harder for businesses to fill positions and for workers to seize opportunities where they are most needed.

Transportation and Infrastructure Barriers

Moving goods across provinces presents another layer of complexity. Trucking companies must adhere to different weight limits, emissions standards, and fuel regulations depending on the province, increasing transportation costs and disrupting supply chains. A truck traveling from British Columbia to Manitoba may need to adjust its load or switch trailers to comply with each province’s distinct regulations. These inconsistencies create inefficiencies that ripple across industries, making domestic trade more expensive and cumbersome than it should be (Canadian Chamber of Commerce, 2021; Macdonald-Laurier Institute, 2020).

Government Procurement and Localized Policies

Provincial governments often favor local businesses when awarding contracts, limiting competition from companies based in other regions. Construction firms, for example, may struggle to bid on projects outside their home province due to preferential procurement policies. Public sector contracts are often structured in ways that prioritize local suppliers, restricting competition and slowing innovation. While intended to support regional economies, these policies inadvertently create trade barriers that prevent businesses from expanding nationally.

Who’s in Charge of Fixing This?

Federal Progress: The CFTA in Action

Responsibility for dismantling these barriers falls on both federal and provincial governments, but progress has been slow. The Canadian Free Trade Agreement (CFTA), introduced in 2017, was intended to reduce trade barriers and align provincial regulations (Canadian Free Trade Agreement, 2024). While the agreement was a step in the right direction, many exemptions still exist, keeping restrictions in place. As of July 2024, the federal government had removed or narrowed 17 CFTA exceptions, with another 20 eliminated by February 2025, reducing federal trade restrictions by 64% since the agreement’s inception (Canadian Free Trade Agreement, 2024).

Provinces, however, have been inconsistent in their approach. Some, like Alberta and Manitoba, have made significant strides.

Provincial Action: Alberta and Manitoba

In 2019, Alberta eliminated 13 of its 27 exemptions under the CFTA, later reducing even more, making it the province with the fewest trade restrictions. Manitoba also removed six exemptions and narrowed another, signaling its commitment to a more open internal market (Canadian Free Trade Agreement, Wikipedia, 2024).

Nova Scotia’s Regional Cooperation Approach

(Image: Cargo ship travelling The Halifax Narrows in Nova Scotia, Canada.)

Nova Scotia has also taken steps in recent years to align with the spirit of the CFTA. While it maintains some exemptions, the province has engaged in ongoing reviews of its regulatory frameworks and has committed to greater transparency by publishing a regularly updated list of its CFTA exceptions. Additionally, Nova Scotia has shown support for regional harmonization through its participation in the Atlantic Regulatory Cooperation Council, which aims to reduce trade frictions among Atlantic provinces and create a more streamlined regulatory environment.

Some provinces have pursued bilateral agreements to harmonize specific regulations, but these remain piecemeal solutions rather than a comprehensive fix.

Conclusion: The Road Ahead

Despite these efforts, significant barriers remain. The CFTA still includes over 160 pages of exemptions, a clear indication that interprovincial trade restrictions are far from resolved (Canadian Free Trade Agreement, 2024). While there is broad recognition of the economic benefits of a more integrated internal market, political will and action may have finally aligned. Canada prides itself on being a nation of free trade, but unless meaningful reform takes place, businesses and consumers will continue to bear the cost of bureaucratic inefficiency and outdated regulations.

If Canada truly wants to unlock its full economic potential, breaking down interprovincial trade barriers should be a top priority. In this US imposed tariff environment, this is one of the low hanging fruits we can deal with to increase productivity and grow the economy.

The question remains—will policymakers step up, or will these obstacles continue to hold Canadian businesses back?

Sources

- UK Patent Box Regime – gov.uk

- Turkey’s Patent Box Regime – WIPO

- Netherlands’ Innovation Box – Wikipedia

- Ireland’s Knowledge Development Box – Irish Times

- OECD BEPS Action 5 – Nexus Approach

- Patent Box Regimes in Europe – Tax Foundation

- UK Patent Box Deduction Formula – gov.uk

- OECD Secretary-General Report to G20 Finance Ministers

- https://taxsummaries.pwc.com/republic-of-korea/corporate/tax-credits-and-incentives

#CanadianEconomy #InterprovincialTrade #EconomicPolicy #USTariffs #TradePolicy #BusinessGrowth #RegulatoryReform #InnovationStrategy #TradeBarriers #CanadaBusiness

Interprovincial trade barriers don’t just limit commerce—they add friction that slows innovation, productivity, and the commercialization of R&D.

At Checkpoint Research, we help businesses navigate regulatory complexity and build strong, fundable R&D strategies—especially when jurisdictional hurdles get in the way.

If you’re expanding across provinces or want to ensure your innovation efforts are fully supported by SR&ED or other funding programs, let’s talk. We turn complexity into opportunity.

8,500

Number of Projects

500M

Total Claim Expenditures

96.5%

Successful Claims